From Triple Lock to Family Support

Phoebe Arslanagić-Little |

Published 28 June 2026

1200

627

1200

627

Phoebe Arslanagić-Little |

Published 28 June 2026

Britain is strongest when each generation keeps faith with the next. Those who have worked hard and contributed all their lives deserve dignity and security in their old age. But those who are starting out or in the middle of their working lives must not be asked to fund a system that will not be there to provide for them in their turn. That is the challenge that this report confronts, with honesty, boldness, and a refusal to pit young against old.

It is widely understood in Westminster that our current pension settlement is under huge pressure and that this pressure is increasing. Our population is getting older, people are having fewer children, and the ratio of pensioners to working age people is deteriorating. The political choice to retain the Triple Lock adds huge cost and a volatile dynamic to this precarious situation.

What happens when younger workers are asked to fund ever mounting costs while, correctly, doubting that the same system will keep them secure in old age? It is a social experiment we should be unwilling to run. At the same time, ending the Triple Lock is likely to be politically very challenging. And so there is cross-party paralysis regarding a policy that is unsustainable and is increasing our national indebtedness, but that is dauntingly difficult to assail. This has become a moral question: we must not allow ourselves to forget that the growing national debt is a claim on the labour, enterprise and earnings of people who do not yet vote and who in some cases have not yet been born. This is yet another reason that getting spending under control and prioritising growth are so vital, not only for us, now. But for them, tomorrow.

Even though reform of the current system will not be painless and must be radical, the answer is not to abandon pensioners. It is to move from a system of unpredictable and ratcheting costs to one based on clear, fair and durable rules, and this report lays out one vision for doing so.

Onward should also be commended in treating pensions policy and family policy as deeply intertwined. That is the reality of our pay-as-you-go system, in which today’s children are tomorrow’s contributors. Making it easier for people to start and raise families is desirable not only because for personal, social and moral reasons we want our country to be a place where good lives can flourish, but because families are central to the long-term sustainability of the state and the support we want to be able to offer at certain times of life.

Establishing a new settlement, that is financially sustainable into the future, that protects the old while commanding the confidence of the young and allowing them to move their lives forward, is a great and necessary task for policymakers in the coming decade. But not an easy one.

Rt Hon Sir Jeremy Hunt MP

Chancellor of the Exchequer 2022-2024

If society is indeed a contract between the living, the dead, and the unborn, then that contract depends on each generation receiving consideration from those who came before and then themselves making provision for those who will come after. Today in Britain, that balance is under mounting strain.

Young people find it increasingly difficult to reach the milestones that have traditionally marked a secure adult life: earning enough to live independently, buying a home, starting a family, and raising children without persistent financial anxiety. Most young people still want children, but many are delaying parenthood or having fewer children than they would like, with financial pressure one of the most important reasons. At the same time, Britain’s population is ageing, the ratio of workers to pensioners is deteriorating, and the cost of old-age entitlements is rising. The result is a growing gulf between the support older generations expect and what younger and future generations will be able to afford.

This is not a zero-sum conflict between young and old and should not be portrayed as such. Older people have contributed throughout their lives and deserve security, dignity and predictability in retirement. Younger people want to start families because children and family life are valuable in themselves, not a mere national socio-economic consideration. But the current settlement compromises both sides of the intergenerational bargain. The State Pension is protected by the Triple Lock, politically attractive but fiscally volatile, increasingly expensive, and difficult for both households and governments to plan around. Pension spending is already one of the largest items in the public budget, and it will rise significantly as the population ages. Under less favourable demographic assumptions, the pressure could be greater still. Meanwhile, government support for families is often poorly timed, too weakly connected to the early years when costs are highest, and insufficiently responsive to the realities of childcare, parental earnings and household financial pressure.

In seeking to address these two problems together, this report from the think tank Onward and the Konrad Adenauer Foundation in the UK also seeks to more tightly bind the fortunes of older and younger people together. It proposes reforms that form the basis of a new intergenerational contract, that sees older people receive the support they need while helping younger people to get a fair start in life. It looks to honour social obligations to those who have contributed to our society and economy all their lives, and make sure that today’s young adults are able to contribute in their turn. Because if we do not fix our fraying social contract, the only certainty is that everyone will lose out.

One in three working-age people say they do not believe that the State Pension will exist in thirty years’ time.[1] In our pay-as-you-go system, wherein those now in work support those now drawing down their pension, that means a large number of people who are paying into the system do not expect to be able to benefit from it in turn.

As difficult as it might be to imagine a world with no pensions or social security for the aged, our current state pension system is indeed threatened by spiralling costs caused by demographic pressures, low growth, and policy choices. The UK’s state pension is the second-largest item in the government budget after health, and the system is so unaffordable that major reforms will be necessary to save it. Though it has become somewhat more common in Westminster to hear this admitted, reform itself has not been forthcoming, with politicians understandably very nervous about floating changes that will make the system less generous for older voters.

But getting ahead of the trends that are making our pension system unsustainable needs action which will take decades to work. That is why the time to act, and to clearly communicate to the public the need for action, is now, even if the problem appears to belong to tomorrow. This section of the report lays out why it is that the State Pension system has become so unsustainable and recommends a package of measures which can help governments to correct our course. Not only will such reforms help to ensure sustainable support for the old far into the UK’s future, over time they can lessen the fiscal burden on governments and help fund the policies we recommend in Chapter 3 to make it easier for more people to start and raise young families.

Older people, who have contributed much in taxes and in other ways throughout their working lives, represent a significant expense to the government, primarily in terms of health, social care, and pension costs. The expense of an older population makes it important that there is a proportionally larger working-age population, working and paying into the system now, and enabling the government to give older people the entitlements and the care that they need.

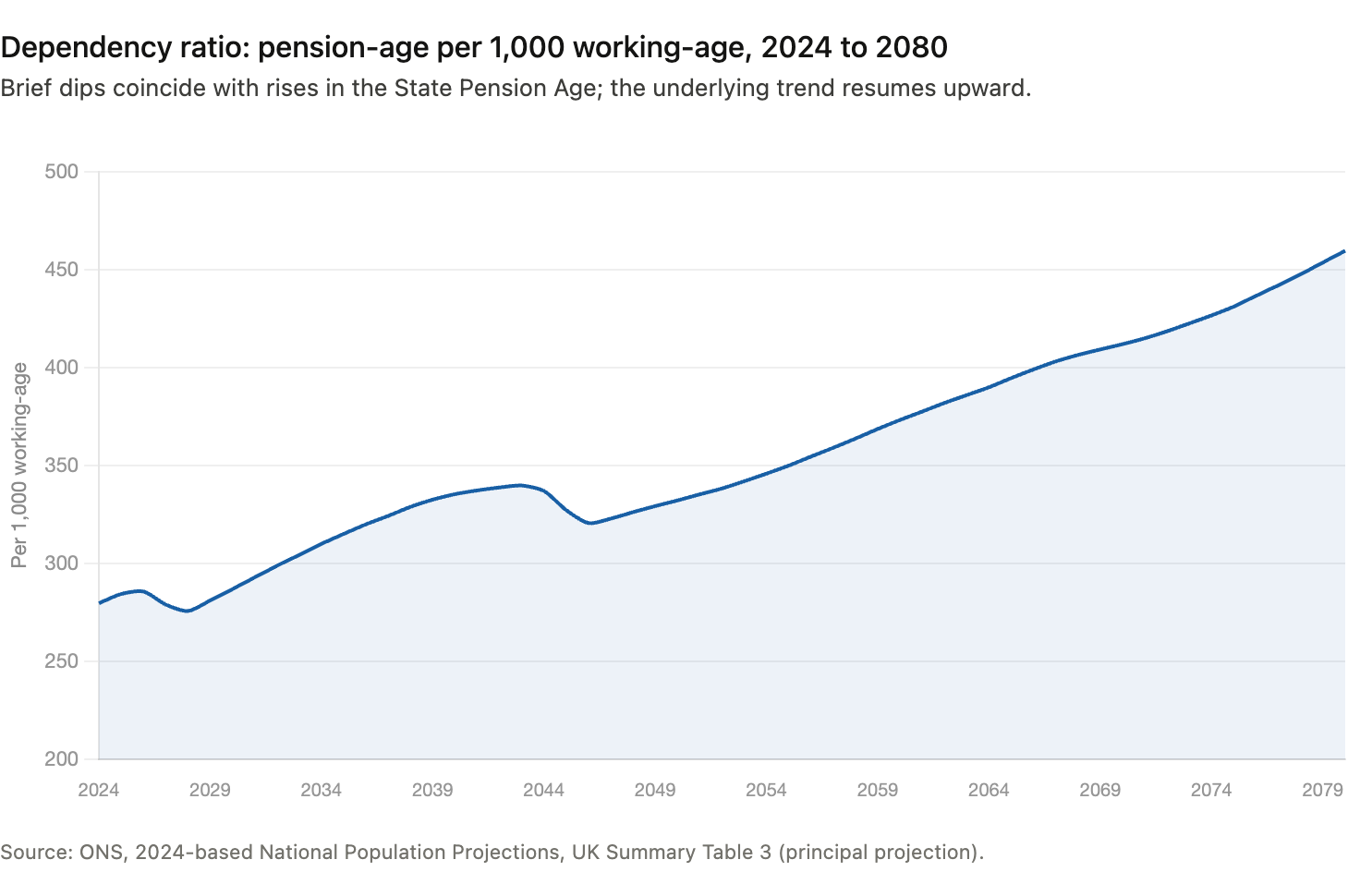

But as Chart 1 below shows, the UK has a rapidly increasing old-age dependency ratio, meaning the ratio of working-age people to those aged over 65. The old-age dependency ratio is by no means a perfect measure, particularly as more of us work later in life. Nevertheless, the very significant increase of the UK’s older population as a proportion of the working-age population does represent a fundamental challenge to the government, particularly in terms of maintaining old age social security.

Chart 1: Pension age persons per 1,000 persons of working age, 2024-80[2]

As discussed above, this is because the UK has a pay-as-you-go pension system, so that the taxes of people working now are used to cover the costs of the State Pension for those who are retired. Fewer working-age people means fewer people paying in to support pensioners who are relying on their State Pension payments.

In 2025 projections based on current policy, the OBR expects spending on the State Pension to rise from 5% of GDP today to 7.7% in the early 2070s.[3] At the current size of the economy, that would see the State Pension costing £213 billion in today’s money, around £75 billion more a year than it does now.[4] That is equivalent to, respectively, more than the entire annual defence budget, more than half of the education budget, and around a third of what we spend on health. This projection assumes that the number of adults of working-age to those above State Pension age declines from 3.4 today to 2.7 by the 2070s, meaning a smaller base of working people supporting higher pension costs. That is the kind of fiscal pressure that will absolutely necessitate some one or combination of significant tax rises, major spending cuts, or even greater levels of borrowing (assuming the latter is even feasible).

However, in making this projection, the OBR must make assumptions about the future, some of which are arguably highly optimistic. In particular, it assumes a TFR of 1.59 births per woman by mid-2045 which then remains at that level.[5] The ONS’s latest 2024 based population projections are already less optimistic, projecting that UK TFR declines to 1.38 by 2029 and then rises to 1.42 by 2049.[6] Since 2010, the ONS’s long term fertility projections have been consistently too high and required revision downward. The UK’s TFR is currently 1.39 and there is no guarantee fertility is about to rebound.[7] As numerous international examples show, it is possible for developed nations to decrease in TFR far below this point and for extended periods of time.

Similarly, and again in line with the ONS at the time in 2024, the OBR assumed net migration of 315,000 a year into the UK in forming its central projection.[8] Already, the ONS has revised this projection down to 230,000 a year from mid-2027.[9] However, much political will exists in the UK, across the political spectrum, for net migration to be much lower.

The ONS itself publishes an ‘old age structure’ of its demographic projections that combines lower fertility, lower migration, and higher life expectancy. In the most recent version of that variant, from 2024, fertility is projected to fall to 1.22 in 2049 and net migration settles at 105,000 a year from 2027.[10]

A simple stress test of the OBR central projection using the ONS’s ‘old age structure variant’ projection shows how State Pension costs could significantly rise under this plausible scenario. Using this official variant, the UK is projected to have just 1.85 working adults per pension-age person by 2073, compared with 2.7 in the OBR’s central projection.

Mechanically scaling the OBR’s projection by that weaker support ratio could push spending from 7.7% of GDP to 11.2%. In today’s money, that would mean a State Pension bill of roughly £310 billion a year, nearing £100 billion more than that in the OBR central projection. That is the equivalent of a government having to find the money to hire an additional two million nurses, or build the Elizabeth Line five times over, every single year.

This should not be read as an alternative OBR forecast. It is a mechanical stress test. It holds constant the OBR’s assumptions about pension generosity, earnings, employment and GDP, and varies only the demographic support ratio.[11] But the exercise is starkly revealing and illustrates how under plausible future scenarios the fiscal burden on the UK from its State Pension as currently designed could be far greater than is centrally projected.

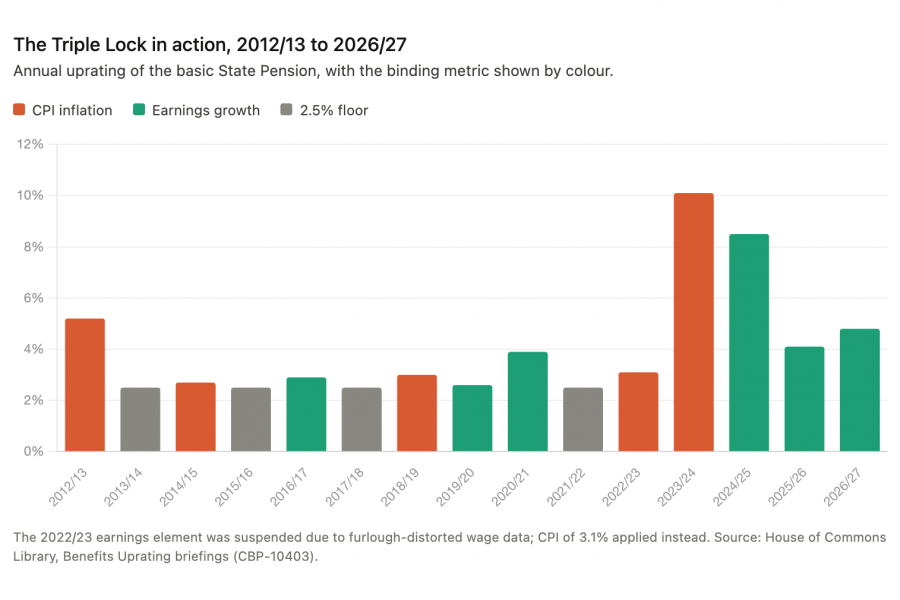

In addition to this demographic pressure, the UK pension system is also strained by the ‘Triple Lock’, a policy which began life in the Liberal Democrat manifesto for the 2010 election[12] and was adopted by the Coalition Government, likely as part of the horse trading of coalition negotiations. The Triple Lock guarantees that the state pension will be increased each year by whichever of the following metrics is highest: earnings growth; inflation (CPI); or 2.5%.

The Triple Lock in part arose as a reaction to what happened when the Thatcher Government decided in 1980 to uprate the State Pension only by prices, breaking the earnings link.[13] This saved successive governments money but meant that pensioners ceased to share in the rising living standards the rest of the country enjoyed. As a result, the State Pension fell from around 26% of average full-time earnings in 1979 to 16% between 2000 and 2010. This state of affairs and worries about pensioner poverty then ushered in the political conditions for the Triple Lock.

Politicians can be forgiven for not having given much thought to the Triple Lock when it was introduced. At the time, wages had persistently outstripped inflation in the past four decades – if the triple lock had been in place for those years, it would have more or less amounted to an earnings link. But a long period of sluggish earnings growth and, in more recent years, high inflation, has made it absolutely unsustainable, leading to very significant jumps in value, as seen in Chart 2 below.

Chart 2: The Triple Lock in action

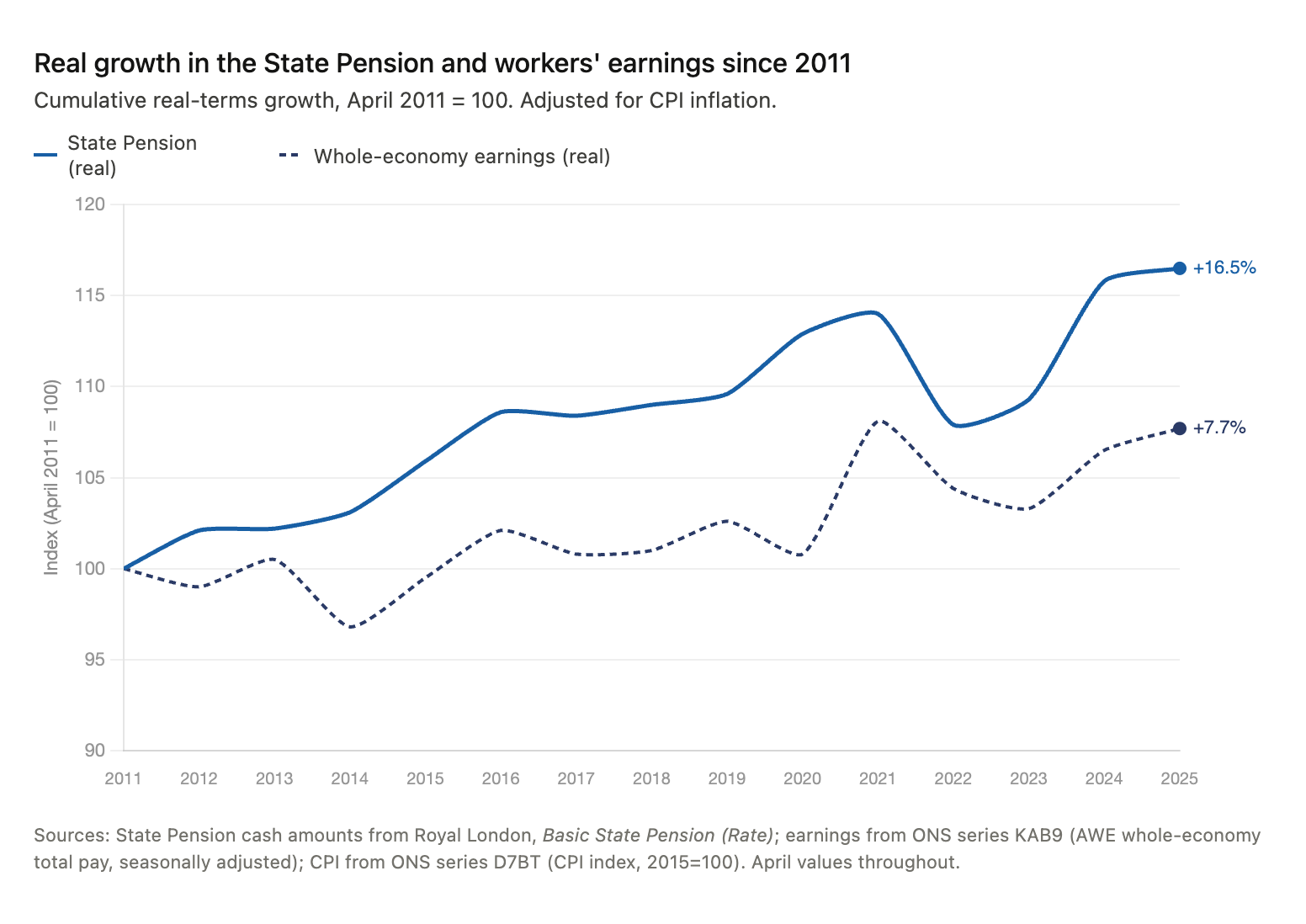

Chart 3: Real Growth in the State Pension and workers’ earnings since 2011

In a further illustration of how serious the implications are for the UK public finances, in 2025, the OBR reported that the cost of the Triple Lock is forecast to be three times higher by 2030 than was modelled at the time of its introduction in 2011.[15] The non-earnings linked element of the Triple Lock had been triggered in eight of the 13 years to date, because inflation “has turned out to be significantly more volatile” than had been expected.[16]

The Triple Lock is a highly politically sensitive topic and politicians have been reluctant to discuss reform, when ever growing numbers of voters are direct beneficiaries of the policy. Because Triple Lock reform has been seen as politically challenging, governments have looked to another major lever in their effort to control cost: raising the State Pension Age. As we live longer, we have to work longer, and adjusting the pension age must play a role in calibrating the system. But there is an argument that the State Pension Age lever is subject to a hard limit in a way that uprating is not. This is because most people can try to do something about the level of their state pension, chiefly saving more during their working lives. By contrast, we can do very little about our life expectancy – it is essentially a fixed factor.

Arguably, the most important test for state-provided, non-means tested retirement income (labelled ‘Pillar 1’ in international pensions literature, with Pillar 2 being private pension saving, and Pillar 3 being means tested help like Pension Credit) is to act as the ‘foundation’ income on which to plan your retirement. Some people have big plans which require lots of money, others want to wind down into a quiet, modest lifestyle. In both cases, knowing how much they need to be saving to hit their retirement goals is mostly dependent on how much State Pension they can expect to be getting. Under the Triple Lock, this is impossible to answer with any certainty.

Firstly, we cannot know with any certainty how long the policy will be in place. It is a political commitment over which the main parties agonise over every five years. Secondly, even if we were certain, the way it operates produces results which will always run ahead of earnings and inflation, but it’s difficult to know how with much certainty. This makes ‘doing the right thing’ quite difficult for savers.

The uncertainty of the Triple Lock also forces the government to be more pessimistic about the cost of social security than potentially it should be, which is bad for the poorest pensioners. Long-term planning is basically impossible under the Triple Lock not just for savers, but also governments that have to administer it.[17] Arguably this means prudent governments have to be very conservative when setting State Pension policy, whereas if the cost was more easily predictable, the public debate around it would likely be on different terms.

Recommendation: State Pension should be uprated according to a Demographics-Adjusted Earnings Link (DAEL)

As described above, the Triple Lock works by increasing the value of the State Pension each year by earnings growth, inflation or 2.5%, whichever is higher. The policy helped to increase the value of the State Pension after decades of erosion and has ensured that pensioners share in rising living standards. However, it is also expensive and highly volatile.

In reforming the Triple Lock, two separate questions should be considered: first what the State Pension should be worth when someone first reaches State Pension age, and second, how the pension should be uprated once someone has retired.

One option for reform, which could control the cost of the earnings link in the long-term, particularly given demographic pressures, would be to only apply it to the value of the State Pension paid in the first year, and only uprate by inflation thereafter. After all, the State Pension is ultimately a benefit: when working-age benefits are uprated it is by inflation in order to protect purchasing power.

However, there is a serious drawback with this reform, which is that over decades of receiving a State Pension uprated only by inflation, pensioners’ living standards will fall further and further behind the living standards of the rest of society. Particularly for those who rely heavily on their State Pension payments, this will mean rising pensioner poverty. To avoid such an outcome, there remains a strong case for retaining an earnings link in some form. The challenge is therefore not to abolish the earnings link but to make it more sustainable.

To meet that challenge, this paper proposes that we retain the principle that the State Pension should rise with living standards, but adjust that link to reflect demographic pressure. In other words, the State Pension will rise in line with earnings but not automatically, or without reference to the number of people who are currently paying for it, a vital consideration in the UK’s pay-as-you-go system wherein today’s National Insurance contributors fund today’s pensioners.

The earnings link should therefore be adjusted or moderated by a demographic mechanism, which would reduce the earnings linked uprating when the base of contributors is weakening or when the number of pensioners is growing faster than the future workforce.

Not only would this demographic slide put State Pensions on a more stable financial footing for the long term, but it would powerfully change the social contract that exists between older and younger voters. Binding the value of the State Pension to earnings and the demographic pressures the country is facing will also bind the fortunes and interests of earners and pensioners more closely together. For example, older voters will be incentivised to support policies that make it easier for young people to start families and be more focused on the barriers such young people face to doing so, including housing shortages or the expense of childcare. Japan has used a similar system since its 2004 pension reforms, using a macroeconomic slide that can respond to a decline in the contributor base or increase in the number of older people.[18]

One way of designing a mechanism for Britain would be through a two-part Demographic Slide, that subtracts measures of demographic pressure from the annual increase in the State Pension generated by earnings growth. The two demographic measures could be:

The Demographic Slide formula could therefore work broadly as follows:

State Pension increase = earnings growth × (1 + weight on the change in the contributor-to-recipient ratio + weight on the change in the new-workers-to-pensioners ratio).

Where the weight is 60/40 in favour of the Current Support Ratio, to reflect its greater relevance to the current fiscal pressures affecting uprating.

However, to prevent the demographic slide from eroding the State Pension to the point that it no longer provides a sufficient foundation for retirement income, the formula should be subject to a floor, so that the value of the State Pension never falls below 28% of average earnings. This allows demographic pressures to moderate the generosity of the earnings link, but still gives people a predictable foundation upon which to plan and save for their retirement.

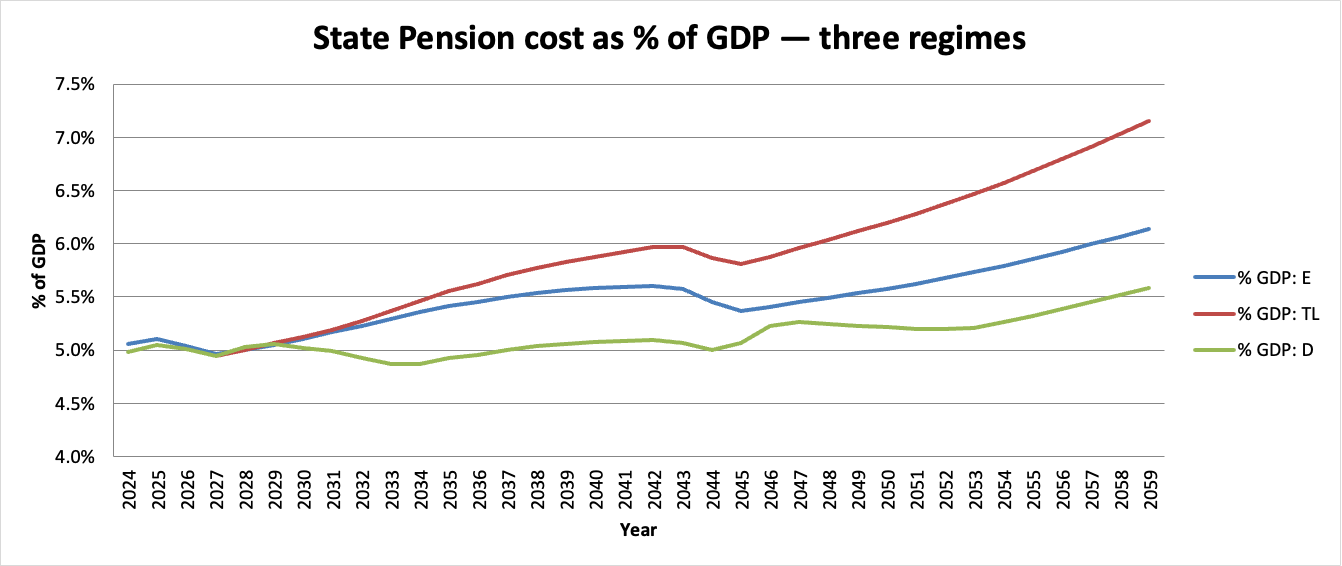

Projections suggest that this policy, of a DAEL with a 28% of average earnings floor, implemented in 2029 to reflect the current political commitment to maintain the Triple Lock until the end of this Parliament, would lead to State Pension spending of 5.58% of GDP in 2060. This is significantly below the 7.1% projected for 2060 with the Triple Lock in place and also below the projected cost of a pure earnings-based uprating (6.14%). By 2060, this policy would save the government around £30 billion a year in today’s money in comparison to a pure earnings link and £86 billion in comparison to the Triple Lock. Crucially, it does so without eroding the amount that the government spends on State Pensions as a percentage of GDP. In purchasing power terms, using the OBR’s CPI projections, it also means a 2060 pensioner is in fact 49% better off than they would have been in 2024.

However, it is important to understand that these projections use the ONS’s principal projection for births, which as discussed in section 2.1, may prove optimistic. In these circumstances, the effect of the demographic slide would be to reduce the uprating of the State Pension, except in circumstances where the 28% floor would kick in.

Recommendation: The State Pension Age setting should cease to be a political decision taken every few years and instead should be set automatically with reference to life expectancy, using a smoothed mechanism that gives at least a decade’s notice of any change.

It is right that as we live longer, we work longer. We already know that our pay-as-you-go public pension system works only as long as the ratio of payers to payees – all things being equal – remains constant. Life expectancy is one of the key factors determining whether or not that is the case, alongside other factors such as the relative sizes of generations.

This does not stop the pension age from being one of the most contested political issues a developed economy with an ageing population can face. Italy’s 2011 Fornero reforms, introduced during the eurozone debt crisis, among other labour law changes sharply increased retirement ages and linked future rises to life expectancy.[19] Feeling against the reforms, the pension elements of which were in part rolled back, ran so hot that the minister whose name they bear was for some time not able to go outside without a guard of ten police officers.[20] Government spending on pensions in Poland is already extremely high, estimated at over 11% of GDP,[21] but with little political will to make cost saving changes like increasing the State Pension age. There is much to lose if such systems buckle under the strain and go bankrupt: state pension payments are the only source of income for 80% of EU pensioners.[22] Variation in average life expectancy by socio-economic characteristics and debates over life expectancy versus healthy life expectancy further muddy the waters when reform is raised.

Today in the UK, setting the State Pension Age is a protracted political process which consumes a huge amount of government bandwidth – it is almost as controversial as the Triple Lock. A key reason for the controversy is because life expectancy rises are increasingly slower than the previous setting cycle anticipated.[23] This gives the Secretary of State for Work and Pensions two options. Either commit to a setting cycle based on out of date life expectancy data (in recent years, likely to have deteriorated) or insist on sticking to the ‘⅓ of life spent in retirement’ commitment, which likely means picking a fight with the Treasury. The end result is – much like with the Triple Lock – that successive ministers are strongly motivated to kick the can down the road. For example, in 2023 the government declined to bring forward the State Pension age rise to 68 and instead left the question for a further review, which was launched in 2025.[24] Yet in many other developed countries, including Finland, Greece, Denmark, Portugal, and the Netherlands,[25] the pension age is set more or less automatically with reference to life expectancy, avoiding major political difficulties.

The UK should move to a similar automated system for setting the State Pension Age, doing so according to a formula that is primarily driven by life expectancy but that also aims for every generation to spend the same proportion of their life in retirement, which is currently around one-third. These changes should be designed to be gradual, with plenty of notice given so that people can plan and save accordingly.

While life expectancy generally is still increasing, those increases have slowed, and the public debate around the last State Pension Age setting cycle centred around this exact fact. Some will argue that the formula should take account of healthy life expectancy, not just life expectancy, as the Tony Blair Institute recently proposed in the form of its ‘Lifespan Fund’ policy, which would use individual characteristics to actuarially personalise access to the state pension.[26] While the concern is understandable, healthy life expectancy is too uncertain and subjective to serve as the trigger for automatic changes to something as important as the State Pension age. Healthy life expectancy varies significantly by region, income and occupation, and is much more difficult to measure consistently than overall life expectancy, requiring unwieldy levels of complexity in any policy that sought to include this measure fairly.

The better approach is to keep the pension-age formula simple and objective, while protecting those who genuinely cannot work longer through other parts of the system. That could include more flexible access to private pensions on health grounds, stronger disability and sickness support, and targeted help for people in physically demanding occupations. The State Pension age should be set by a clear demographic rule; hardship and ill health should be addressed directly, not by making the whole formula less stable.

The government should commission an independent expert review to design a smoothed automatic mechanism for setting the State Pension Age, with a guarantee of a minimum of a ten years’ notice before any change takes place and using rolling averages of life expectancy projections to prevent short-term shocks causing major swings in the timetable.

A strong objection to Triple Lock reform flows from the desire to prevent increases in pensioner poverty and protect the pensioners who depend the most on their State Pension. But this is ultimately an argument for strengthening Pension Credit, not preserving the Triple Lock and all its problems.

Pension Credit is the part of the pension system that is specifically designed and intended to protect the poorest pensioners and played a very significant role in reducing pensioner poverty in the 2000s.[27] It is formed of two parts: Guarantee Credit, which is a means-tested element that tops up pensioners’ weekly income; and Savings Credit, which is a smaller additional payment for some pensioners who reached State Pension age before April 2026 and is not closed to newer pensioners. Currently, the problem with Pension Credit is that it does not reach enough of the people it is supposed to: in 2023 to 2024, only 62% of those entitled to the benefit received it, leaving up to £2.5 billion unclaimed, on average around £2,600 per year per eligible family.[28]

To fix this problem and make sure Pension Credit is working as it should, the government should move towards automating Pension Credit awards. This can be done in two steps:

First, the capital rules should be simplified. Savings and investments above £10,000 reduce the award. But this rule makes automation much harder, because DWP cannot determine a claimant’s capital holdings without asking them what they are. Removing this requirement would be the simplest reform and would mean that HMRC and DWP know everything they need to know about whether someone is eligible for Pension Credit without a proactive application necessary. After all, Pension Credit is aimed at pensioners with very low weekly incomes and those whose incomes are low enough to qualify but have substantial liquid savings are unlikely to be a large group. However, this can be tested using the Family Resources Survey and DWP administrative data.

Second, HMRC should automatically share an applicant’s income details with DWP when they apply for the State Pension. This will enable DWP to automatically add Pension Credit to that applicant’s State Pension payment, thus removing the need for the eligible pensioner to apply.

Together, these measures can ensure that even as the Triple Lock is removed, more of the poorest pensioners are receiving the help they need and are intended by the government to receive. Finally, it is also the case that factors such as the introduction of pension auto-enrolment and the very significant increase in female labour market participation mean that the number of people who need to and will need to rely on Pension Credit is diminishing over time.[29] This declining caseload may mean that, in time, the government can consider simply withdrawing Pension Credit.

The three reforms laid out above are intended to stabilise and strengthen the UK’s existing pay-as-you-go public pension system. A further question is whether the UK should supplement that system by creating a pension reserve fund.

As laid out above, currently the UK system works by using National Insurance contributions and wider tax revenues raised from the current working-age population to fund State Pension payments to the current generation of pensioners. Workers do this on the implicit understanding that the next generation will do the same for them. Now, because of people living longer, falling birth rates, and a greater share of the population reaching retirement, this system has become unstable.

The proposed response of this paper has been to adjust the pay-as-you-go system itself, by automating the State Pension age and changing uprating policy. But a further reform that could be introduced would be to build a reserve fund in advance, so that some of the cost of future pensions is met not only by future workers, but also by investment returns accumulated over time. Around the turn of the century, a number of developed economies established funds of this kind, including France, Japan, Australia, New Zealand and Ireland. Their designs differ, but the core principle is similar: set aside public money, invest it in a diversified portfolio of higher-return assets, and use the proceeds at a future date to help support the public pension system during a period of pressure, thus smoothing out the pressure on younger and future generations. The UK has not taken this route, and an opportunity to establish a sovereign wealth fund was arguably missed in the 1980s, when revenues from North Sea oil were at their height. Instead, the Thatcher Government explicitly chose to return that revenue to the public in the form of tax cuts.

But a UK reserve fund does have an attractive intergenerational logic. It would allow the state to convert a temporary fiscal windfall into a permanent asset, with the returns used to reduce future pressure on taxpayers, workers and pensioners. It could also make the pension system less reliant on repeated political adjustments to the triple lock, the pension age or National Insurance. If created, such a fund should be managed independently, invested in a highly diversified manner, probably best globally, and with strict governance to avoid political interference.

While the UK does have a National Insurance Fund that technically invests its surplus, it is obligated to invest that surplus almost entirely in gilts.[30] This means that in practice, this money is lent to the government, at an interest rate near the Bank of England base rate, for general spending purposes. Repurposing any part of that money, therefore, would amount to raising the government’s borrowing requirement by that amount. In other words, the ‘surplus’ isn’t really a surplus, because it already is being used for something. If the money were diverted from gilts into equities, infrastructure or other higher-return assets, the government would need to borrow more elsewhere to replace it. This amounts to borrowing to invest.

Borrowing to invest is not automatically wrong. There are circumstances in which it can be justified. But it creates a demanding test: the fund must be expected to earn more than the government’s cost of borrowing, and by a sufficient margin to compensate for risk, volatility and political constraints.

That is a difficult test today. With gilt yields elevated, the return hurdle for a new UK fund is much higher than it would have been in the 2010s. If the Government can borrow at around 5%, and a conservatively managed long-term fund might be expected to earn around 6% nominally, the expected spread is thin. A one percentage point margin may not justify the risk of using scarce fiscal capacity to invest in markets rather than reduce borrowing, cut taxes or fund public services.

This is why sovereign wealth funds and public pension reserve funds have traditionally been thought most suitable for countries with budget surpluses, natural resource revenues or major one-off windfalls. For countries with persistent deficits, the policy can look less like saving and more like leveraged investment. In the words of Paul Goldsmith, New Zealand finance minister arguing that payments to New Zealand Super Fund, the country’s PPRF, should be suspended because the country cannot afford them: ‘If it was a slam dunk, we may as well borrow a half a trillion dollars and give it to the Super Fund. It’s not a slam dunk.’[31] However, this has not stopped several countries with large deficits from establishing such funds in recent years, including Ireland and Canada.

A UK pension reserve fund would need to reach £300-£600 billion at maturity to deliver £15-£30 billion a year in drawdowns (roughly 10-20% of today’s State Pension cost). Working backwards from this with the sort of growth profile the model can produce – 6% annual return, 25 years of accumulation – implies a present-value seed somewhere around £80-£200 billion, or a smaller seed (£20-50 billion) plus very substantial annual contributions for more than 25 years.

There are a number of ways a government could find the money to create such a fund, including by using the National Insurance Fund surplus, though as discussed this is essentially funding through borrowing. Perhaps the least painless way for a nation to seed its reserve fund is through windfalls, such as might be generated via the selling of government assets such as land. This is what the Trump Administration says it intends to do for its proposed Sovereign Wealth Fund. Alternatively, the fund could be seeded through the levy of a new, hypothecated tax, though this would raise questions from the many voters who believe their National Insurance contributions are already going to fund their future retirement.

It may be the case that the specific conditions the UK currently faces, not least surging gilt yields and a rapidly growing national debt, mean that there are simply too many opportunity costs to allow a reserve fund to be established. However, when conditions permit, or in the event of windfalls that could seed such a fund, it would be wise for the government to strongly consider establishing one.

In this section, we propose three policies aimed specifically at making life better and easier for new parents, through changes to the tax, social security, and childcare systems. These policies are neither a ‘reward’ for people who have children nor a punishment for people who do not want to, or cannot, start a family. They recognise the fact that children, every single one of whom is important in their own right, are a contribution to our future national prosperity even as they are expensive to raise. In other words, because we all benefit when people choose to have children and so we all benefit when policy makes it easier for people to do so.

This is particularly a matter of concern because the Total Fertility Rate in England and Wales is 1.39 In Scotland – due to start depopulating in less than a decade’s time – it is just 1.25, on par with famously low fertility Japan.[32][33]

As fertility falls and life expectancy rises, the ratio of retired to working-age people increases. This places growing fiscal pressure on the working-age population, as a larger share of government revenue is required to fund healthcare, pensions, and social care for an ageing population. Core elements of Britain’s social infrastructure, including the NHS, were designed for a much younger society. Without demographic renewal, their long-term sustainability is in question.

The immigration of working-age people mitigates an increasing old-age dependency ratio, more quickly but less durably than more children being born. But even after the very high levels of immigration the UK has experienced over the past decade, our old-age dependency ratio has continued to increase. With increasing political and democratic consensus that immigration to the UK must come down very sharply, we can expect the mitigating effect of working-age immigration to lessen over the coming years.

Low fertility also constrains economic growth. An older population absorbs more public spending, limiting investment and reducing disposable income through higher taxes. Over time, fewer births mean fewer workers and lower output. And because innovation depends on people, demographic decline ultimately weakens the ideas and dynamism on which growth depends: for there to be ideas, there must be human beings.

Taken together, it is vital that the British government does not remain neutral on whether or not people have children. Instead, policymakers must make life easier for British people to start, grow, and support their families. Furthermore, there is strong evidence that British people are having fewer children than they would like to have.

While the British state already supports parents, through universal provision like education and targeted measures such as Child Benefit, children remain materially costly for individual families, even though they generate large social returns. The costs begin before birth: equipment such as prams, cots, and car seats is expensive, while caring for young children significantly reduces parents’ earning capacity. Mothers in particular are likely to take time out of the workforce in a child’s first year, and even with the aid of government-subsidised childcare provision, parents face constraints on working hours that persist well beyond infancy.

These pressures help explain why households with dependent children are much more likely to experience financial difficulty than those without. Survey evidence[34] consistently shows that financial insecurity is a major factor deterring people from having children they want, whether that means postponing parenthood or deciding against another child.

Taken together, the policies proposed in this section focus on the period when children are youngest. The financial pressures associated with parenthood are not evenly distributed across childhood. They are heavily concentrated in the early years, when parents’ earning capacity is most constrained and childcare costs are highest. The reforms outlined below aim to rebalance support towards this phase of family life, reducing the upfront financial shock of having children while also making it easier for parents to remain in work.

One way to recognise the social value of raising children is through the tax system. While the government provides transfers to families through benefits and services, the structure of taxation itself remains almost entirely individualised. This means that the tax system does little to recognise that households raising children face higher costs while having lower effective earning capacity.

Should parents pay less tax? This paper argues that they should. Specifically, we propose that those who are raising young children should pay less income tax, making it easier for these parents to raise their young families.

Despite the extra costs borne by parents, especially when children are young, the British tax system takes no account of family responsibilities. Two adults earning the same income pay the same tax, even if one is supporting children and the other has no dependents. This ignores both the social value of children and parents’ reduced ability to pay tax.

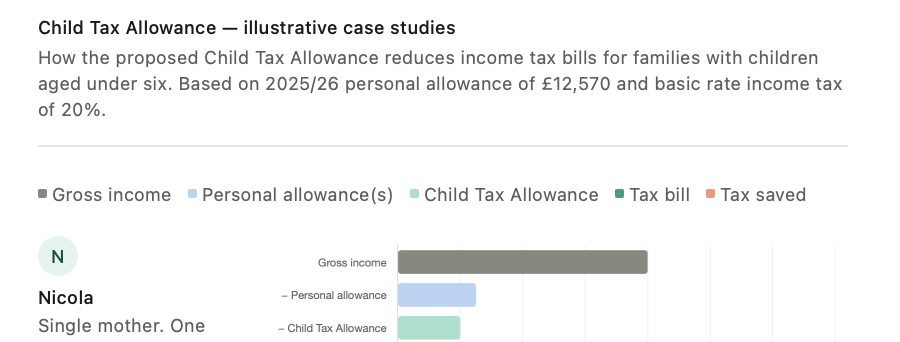

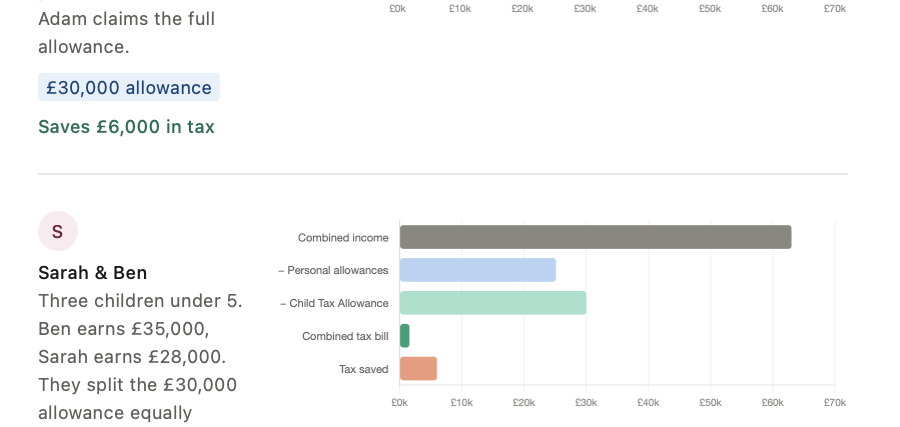

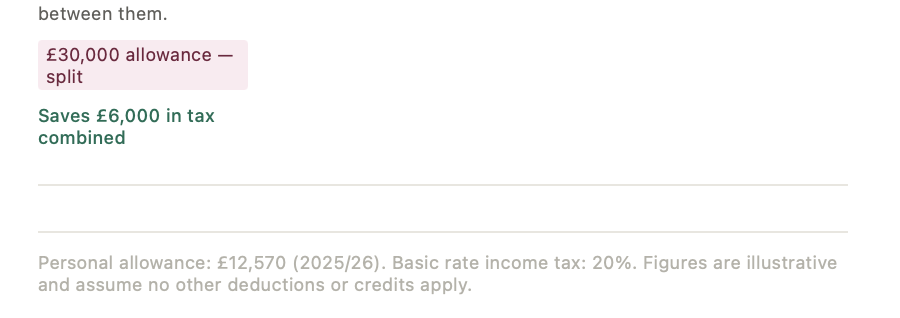

In recognising this reality, a Child Tax Allowance could ease the financial burden of raising children, making it easier for people to form and expand families in the first place.

We propose a basic rate Child Tax Allowance of £10,000 per child aged under five, £20,000 per two children under five, and £30,000 per three or more children under five. This would effectively increase the amount that parents of children aged under five keep of what they earn. This Allowance would be worth up to: £2,000 for a household with one child aged under five; £4,000 for a household with two children aged under five; and £6,000 for households with three or more children aged under five. Because the relief of the Allowance would only be applied to basic rate income tax, the Allowance would function much like an increase of parents’ personal tax allowance. Parents or primary caregivers would be able to choose to split the Allowance between themselves or have it applied to one income only. We estimate this policy would cost £4.8 billion a year, assuming that every two-parent household opts to split the Allowance between them in a tax efficient manner.[35]

These hypothetical case studies illustrate how the Allowance would work for families:

It is important to note that the splitting element of our Child Tax Allowance policy would currently be very complicated for HMRC to administer, because it lacks data on families. A version of the policy that applies it only to one parent’s income would be significantly easier to administer with data the government currently has access to, and would also be cheaper. However, it would also mean more eligible parents keeping less of their earned income.

Reducing the tax burden on parents addresses one dimension of the cost of raising children. But financial transfers alone cannot resolve the practical constraints that many parents face when attempting to combine work and family life. In particular, access to reliable childcare remains one of the most significant barriers preventing parents from returning to work or increasing their working hours. Addressing this constraint requires reforms not only to financial support, but also to the childcare system itself.

Parents in England face restricted access to childcare in terms of both cost and availability. The government’s free childcare offer expanded in September 2025 but there has not been the necessary increase in spaces to be able to accommodate the ensuing increased demand, especially as shortages existed before the expansion. At the same time, there is a long-running decline in the number of childminders in the UK. Difficulties finding the right childcare makes it more difficult for the parents of young children, especially mothers, to work or increase their hours. Yet, the government does very little to encourage another, very popular type of care: the informal care provided by trusted relatives like grandparents.

Under the government’s current free childcare offer,[36] working parents with a child aged between nine months and five years old are entitled to 15 free hours of childcare a week during school term time. The parents of all three to four year olds are entitled to 15 hours of free childcare a week and working parents to 30 hours a week during school term time. As of September 2025, the government’s free childcare offer increased in generosity: now, 30 hours of free childcare a week is available for eligible working parents with a child from nine months old up to school age, during school term times.

But in 2024, before the offer expanded in generosity, less than half of English local authorities reported[37] having enough childcare places to meet the entitlement. Only 45% said they had sufficient provision to meet the current 15 hour entitlement for two year olds, and 62% said they had enough provision to cover the 15 hour entitlement for three and four year olds. Between December 2024 and December 2025, the number of registered childcare places in England increased by only 15,800, a far cry from the 85,000 new places that the Department for Education estimated would be necessary by September 2025.[38][39]

A contributing factor to the anaemic increase in places is the sharp decline in the number of childminders. Between 2013 and 2023, the number of childminders in England declined[40] by over 50%. Between 2024 and 2025, over a thousand childminders left the sector.[41] The decline in childminders also means available formal childcare has become less flexible, as childminders are often able to be more flexible and offer services like wraparound care.

For parents, England’s childcare shortage places means long waiting lists[42] for places and long journeys to settings that do have availability. Government analysis finds that access to childcare has declined overall in England since 2020, but that the decline is regionally concentrated[43], with the North East, the East Midlands and Yorkshire and The Humber seeing the largest proportional decrease in their childcare access over this period. However, there is also evidence that parents in London are more likely to struggle to access childcare, with 65%[44] of mothers in London with a child aged under ten struggling to find childcare, compared to 54% across the UK.

This matters because access to childcare is a key factor affecting the ability of parents to work: more people enter the workforce where access to childcare improves. 2023 analysis[45] found that the government’s introduction of 30 hours a week of free childcare for all working parents of three and four year olds led to around 286,000 more people in employment a year on and an increase of £22.3 billion in Gross Value Added. Equally, poor access to childcare has negative labour supply effects and England’s childcare shortage is making it more difficult for the parents of young children to work or increase their hours.

In England, there is a significant cohort of parents of young children who would prefer to work if they had access to the right childcare. In 2023, 54% of non-working mothers with children aged 0 to 4 said[46] that if they could arrange good quality childcare that was convenient, reliable and affordable, they would prefer to go out to work.

But this effect is not felt equally between parents, with mothers more likely than fathers to struggle to return to work or increase their hours where there are difficulties finding childcare. Mothers themselves clearly identify this difficulty as making it harder to work. 2023 polling[47] of UK mothers with at least one child aged under ten found that 46% of those who reported struggling to find childcare said this challenge had prevented them from working more hours. 29% said they had reduced their working hours as a result of struggling to find care.

Expanding formal childcare provision is one response to this challenge, but it is not the only one. A large share of childcare in Britain already takes place outside formal settings, provided by relatives and trusted adults. Yet this informal care receives almost no recognition in public policy, despite playing a crucial role in enabling parents to work.

Currently the only government scheme to incentivise and support informal care allows grandparents providing childcare to working parents to claim National Insurance credits in order to help fill gaps in their National Insurance record. The scheme[48] is restrictive and uptake is low[49]: credits are only available to grandparents under state pension age and the value of the scheme is limited to £6,000 over the entire course of retirement. There is zero government support for the informal childcare provided by other trusted adults, such as aunts and cousins.

But the informal care provided by grandparents and other close relatives is an important form of childcare that helps parents, especially mothers, go out to work. In England in 2023, 48%[50] of working mothers with pre-school children identified having relatives who can help with childcare as a factor that helps them to work. Grandparents are the key providers of this informal care – 28% of grandmothers and 16% of grandfathers report[51] caring for their grandchildren, at an average of just over eight hours a week.

Beyond the reports of young mothers, evidence does show that access to grandparental childcare helps mothers work. Cross-country European research shows[52] that when grandparents care for young children they increase the likelihood that the mother of those children works by 13 percentage points, and that the effect is most significant for mothers of pre-school children.

But even as the number of young mothers returning to work has increased over the past few decades, the average hours of childcare provided by grandparents and the proportion of grandparents providing such care has not increased[53]. There have been no policy attempts to encourage more grandparents to provide more childcare.

Rather than relying exclusively on the expansion of formal childcare provision, government policy should also recognise, support and incentivise the informal childcare that already underpins the childcare system. By allowing parents to allocate part of their childcare entitlement to trusted caregivers such as grandparents, the state could expand the effective supply of childcare quickly and at relatively low cost.

We propose that working parents should be able to use their free childcare entitlement to compensate the informal childcare provided by trusted adults like grandparents, which would require an amendment to the Childcare Act 2016.

To be eligible for this expansion in the scope of the free childcare entitlement, parents would need to meet the work and minimum earnings requirements of the 30 free hours childcare entitlement. This would mean that both parents must be in work, and earning on average the equivalent of 26 hours a week at the national minimum or living wage. However, parents should not lose eligibility if their income exceeds £100,000 – this is in order to protect incentives to work and maximise the labour supply effects of the policy change.

To make use of this policy change, parents would continue to apply online to register for the entitlement but will also be able to allocate some or all of their 30 hours to their named trusted adult. Parents would need to apply with: the name and address of the trusted adult and their relationship to them; and an enhanced DBS check with barred lists for the trusted adult.

We anticipate that the vast majority of trusted adults would be grandparents or other close relatives. The hourly compensation rate provided by the government would reflect that this informal care is not equivalent to that offered by EYFS-qualified nursery staff and childminders and so will be set at a rate lower than that awarded to nurseries and childminders, initially at £5 an hour. To protect high standards of care and reduce the chance of fraud, no one trusted adult will be able to be registered as and receive compensation for caring for more than four children.

The compensation should be delivered via a tax credit for parents, who can then pass the compensation on to the trusted adult. For employed parents, the tax credit would be administered via PAYE, so that trusted adults may be compensated on a monthly basis. Self-employed parents would need to claim the tax credit via their yearly self-assessment. The named trusted adult should themselves receive regular email communications informing them when the compensation has been issued to parents and how much has been issued.

This policy change would enable more grandparents to care for their grandchildren, and to do so for more hours, by recognising the value of the childcare that they do and contributing to costs[54] incurred in providing this care. This policy can also encourage other trusted adults, such as aunts, uncles, cousins and close family friends, to increase the childcare support they give to parents now.

Encouraging the highly flexible care that grandparents and other trusted adults can provide would help to ameliorate England’s childcare shortage. This policy can also achieve these goals at a lower cost to the Treasury than purely subsidising the formal care provided by nurseries and childminders. This is because the care provided by grandparents and other such trusted adults is informal and not equivalent to that offered by qualified nursery staff and childminders. To reflect that, the hourly compensation rate should be below that awarded to formal settings.

Compensating grandparents for childcare can help address the childcare shortage by enabling more grandparents to care for their grandchildren, for more hours, and at a lower cost to the government than the formal care provided by nurseries and childminders.

The economic impact of this policy will be multifaceted. The main objective of the tax credit is to incentivise grandparents or other trusted caregivers to provide additional childcare. But from an economic standpoint, this could have effects through three different channels.

The reforms discussed so far focus on reducing the tax burden on parents and improving access to childcare. But the structure of direct financial support for families also matters. In particular, the timing of government support can influence family formation decisions and the financial pressures experienced by parents when children are youngest.

Child Benefit is a means-tested payment that sees eligible parents receive payments every four weeks, per child. Even after 2010 reforms that have limited eligibility, Child Benefit is an expensive and generous benefit. But changes to how and when Child Benefit is received by families could transform its impact and value to parents.

Child Benefit can only be claimed by one parent and is currently worth £26.05 a week for an eldest child and £17.25 a week for an unlimited number of further children, paid out on a monthly basis. A parent can claim Child Benefit until their child is 16, and until 18 if they stay in full-time education. Child Benefit has been means-tested since 2010, through the High Income Child Benefit Charge (HICBC). The form taken by HICBC today means that if anyone in a child’s household earns above £60,000, Child Benefit payments begin to be tapered away, diminishing to zero once anyone in the household is earning £80,000 or more. Onward has previously called for the abolition of HICBC, which contributes to severe effective marginal tax rates for many families.[55]

Child Benefit is expensive, costing the government £13 billion a year, and it is worth a lot to parents. For an eldest child who stays in education until they are eighteen, a household can expect to receive over £24,000 in payments in total, and a little over £16,000 for a second child. That is a significant sum of money, but spread out over a long period of time. That is despite the fact that children are particularly expensive to their parents when they are pre-school age, because the care they require impedes their parents’ ability to work and because of the cost of childcare.

The amount of financial support that new parents receive is particularly important to helping them realise their desired number of children. Personal financial outlook and stability is a key factor that influences when and how many children parents and prospective parents choose to have. That means that support given around the time that these decisions are being made, particularly the decision to have a second or third child, is disproportionately effective in helping parents to decide to have wanted children.

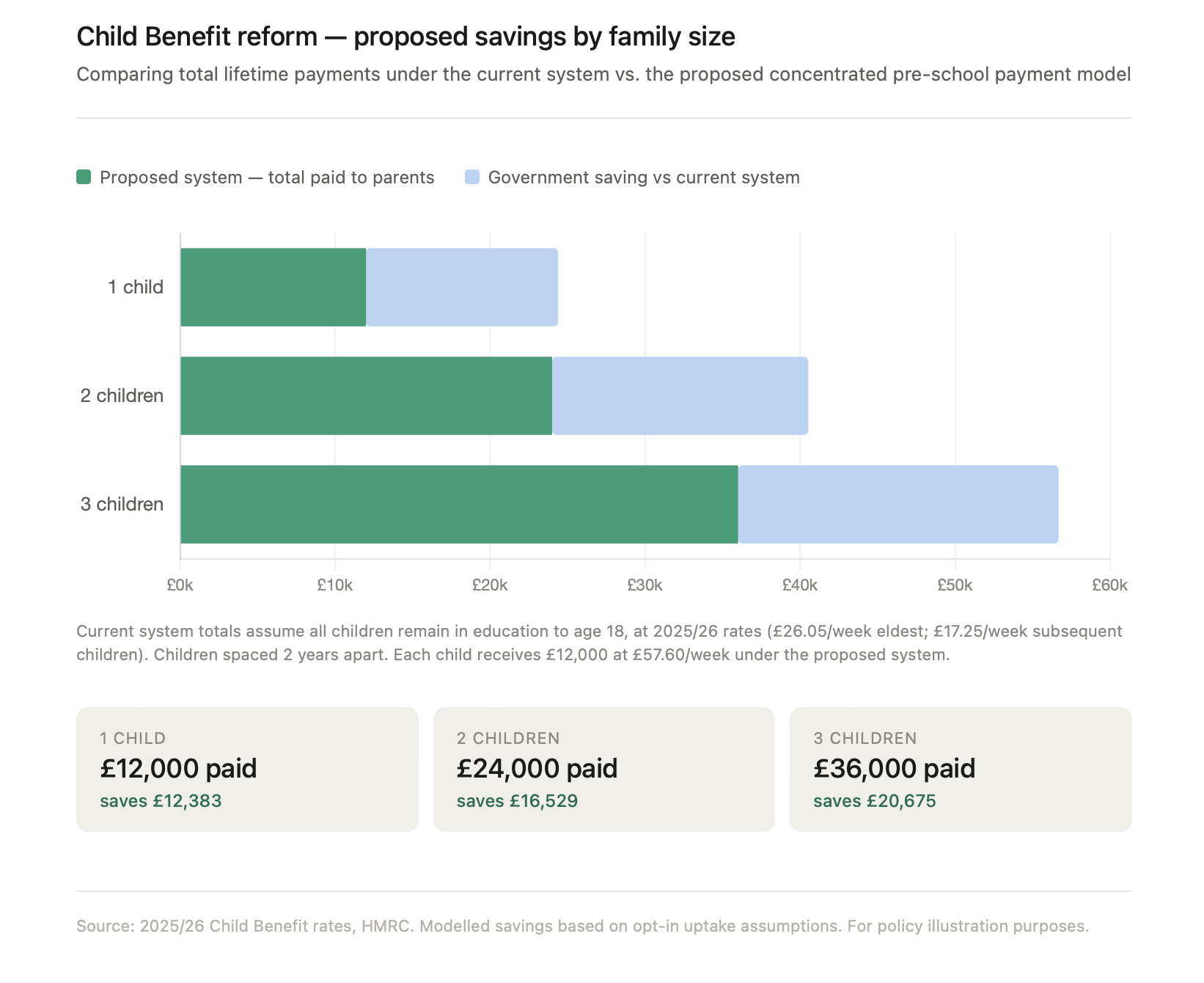

In addition to giving Child Benefit payments piecemeal over a sixteen or eighteen year period, the government should also allow eligible parents to opt into a new system that will see them receive a smaller amount of money but concentrated over the much shorter period before their child starts school.

We propose that, as an alternative to receiving £26.05 a week for an eldest child and £17.25 for any subsequent child, parents opting for the new system instead receive £57.60 per week for all children aged under five. Overall, this will mean that these parents receive £12,000 in Child Benefit payments for each of their children, at a time in life when their children are particularly expensive to them.

Chart 4: Child Benefit reform – proposed savings by family size

The government would also save money for every parent who chose to take up this new system. As the chart above shows, the government would save over £12,000 for every oldest child whose parents opt into the new system, and a little over £4,000 for any second and subsequent children who choose the new system.

This hypothetical case study illustrates how the new system could help young families.

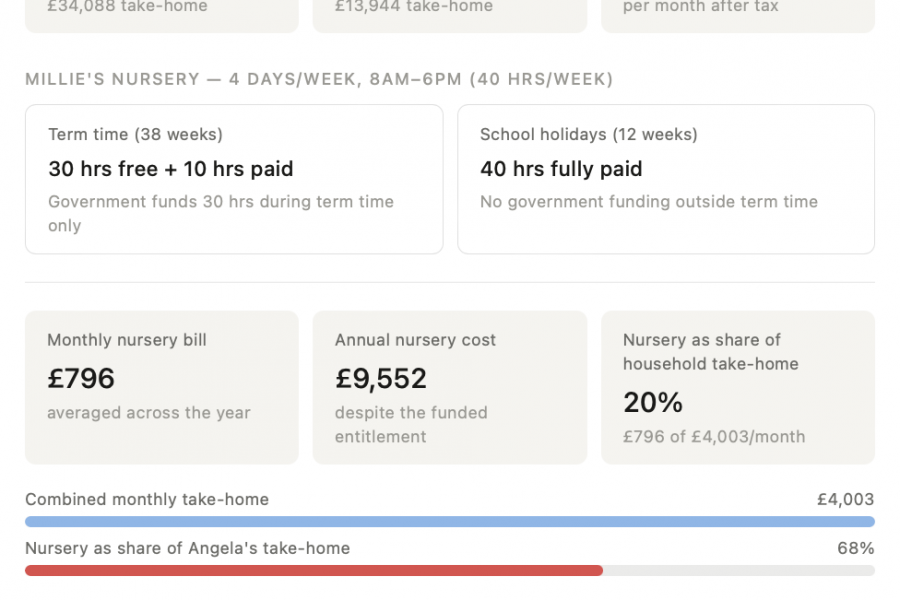

George and Angela live in north London with their daughter, Millie, aged two. George works full time and Angela works four days a week. Millie goes to nursery four days a week, from 8am to 6pm. As eligible working parents, George and Angela benefit from 30 hours a week of government-funded childcare. But they actually use 40 hours a week and the 30 free hours only apply to 38 weeks of the year, during school term time. To cover those extra hours, they pay for 10 hours on top of the funded entitlement and for the full 40 hours for 12 weeks of the year. That means that despite subsidised childcare, George and Angela spend £796 a month on childcare, or £9,552 a year.[56]

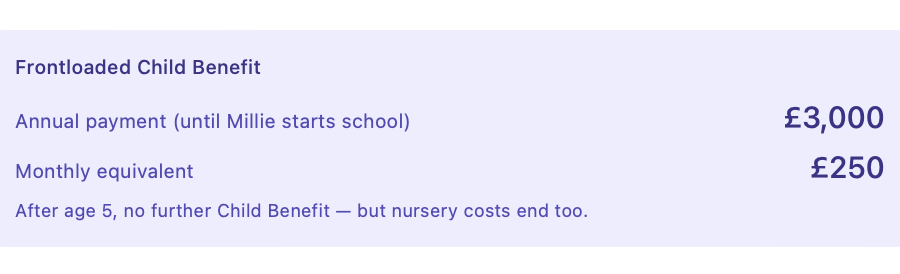

George and Angela opted into the new Child Benefit system when Millie was born and will receive £3,000 a year in Child Benefit until Millie starts school. This money has been very helpful in making their childcare bill more affordable and helped Angela to decide that it was worth her while to return to work. Initially, she was not sure it would be as she only takes home £13,944 post tax from her salary of £30,000, and nursery fees take up 68% of that. And during the first year of Millie’s life, the family found the extra Child Benefit very helpful in meeting household expenses while Angela was only receiving Statutory Maternity Pay.

The couple are aware that receiving the enhanced level of Child Benefit means they will not be eligible for any Child Benefit at all once Millie is aged five. But they are not concerned about that because the extra money is so helpful in meeting childcare costs which they know will not be an issue once Millie starts school.

It should be clearly stated that though this reform would indeed save the government money over time, it would have implications for the government’s near-term financing requirements, because Child Benefit expenditure is being brought forward. This higher upfront spending is likely to raise gilt yields, thus putting up the cost of government borrowing. This is a real risk and should be mitigated by proposing this policy alongside cost-saving measures, including those proposed in Chapter 3 but also potentially wider reforms to the benefit system.

This report has argued that pension reform and family support should be understood together as part of the same agenda. The common principles that underpin that the proposals are reciprocity and sustainability.

The pension reforms this paper proposes seek to protect pensioners from inflation and ensure they share in rising living standards, while reflecting real demographic pressures. Increases to the State Pension age would become significantly less politically fraught and more predictable, allowing people to plan. And the poorest pensioners would be protected in a targeted way through a strengthened Pension Credit system rather than through an expensive universal Triple Lock. When fiscal conditions allow, a pension reserve fund could help future governments smooth the costs of ageing across generations and further stabilise the State Pension system.

But Britain must also make it easier for people to start and raise families. The policies proposed in this report are deliberately focused on the early years, when the financial shock of parenthood is greatest and parents’ earning capacity is most constrained. A Child Tax Allowance would recognise that parents of young children have a lower ability to pay tax than otherwise similar households without dependents. Compensating informal childcare would make better use of the trusted care already provided by grandparents and other relatives, while helping parents return to work or increase their hours. Frontloading Child Benefit would give families more help when children are young, without necessarily increasing the lifetime cost of support.

The aim is not austerity for the old or unlimited subsidy for the young. Moving from Triple Lock to family support must mean reform that is honest about our fiscal future if politicians fail to act to solve the unaffordability of our current pension system or face the challenge of the demographic pressures we are already experiencing.

[1] Cribb, Emmerson, and Barker, “The Pensions Review”, Institute for Fiscal Studies (2023). https://ifs.org.uk/sites/default/files/2023-12/IFS-R291-The-future-of-the-state-pension.pdf

[2] UK Summary Table 3 from the “National population projections: 2024-based”, ONS, https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationprojections/bulletins/nationalpopulationprojections/2024based (2026).

[3] “Fiscal risks and sustainability – July 2025”, Office for Budget Responsibility, https://obr.uk/frs/fiscal-risks-and-sustainability-july-2025/ (2025).

[4] “Welfare spending: pensioner benefits”, Office for Budget Responsibility, https://obr.uk/forecasts-in-depth/tax-by-tax-spend-by-spend/welfare-spending-pensioner-benefits/ (2023); Cash figures are Onward calculations applying the OBR’s projected GDP shares to the current spending of £138 billion.

[5] “National population projections, fertility assumptions: 2020-based interim”, ONS,https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationprojections/methodologies/nationalpopulationprojectionsfertilityassumptions2020basedinterim(2022).

[6] “National population projections, fertility assumptions: 2024-based”, ONS, https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationprojections/methodologies/nationalpopulationprojectionsfertilityassumptions2024based(2026).

[7] “Births in England and Wales: 2025”, ONS, https://www.ons.gov.uk/peoplepopulationandcommunity/birthsdeathsandmarriages/livebirths/bulletins/birthsummarytablesenglandandwales/2025, (2026).

[8] “Net migration forecast and its impact on the economy”, OBR, https://obr.uk/box/net-migration-forecast-and-its-impact-on-the-economy/ (2024).

[9] “National population projections: 2024-based”, ONS, https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationprojections/bulletins/nationalpopulationprojections/2024based (2026).

[10] “Dataset – Old age structure variant – UK summary”, ONS, https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationprojections/datasets/tablel11oldagestructurevariantuksummary (2024).

[11] This is a mechanical stress test, not an alternative OBR forecast. The OBR’s central projection has State Pension spending reaching 7.7% of GDP in the early 2070s, with around 2.7 adults below State Pension age per pensioner. The ONS’s 2024-based old age structure variant projects that, by 2073, the UK will have 35.7 million working-age people and 19.3 million pension-age people, equivalent to 1.85 working-age adults per pension-age person. Holding the OBR’s assumptions about pension generosity, earnings, employment, productivity, GDP and policy constant, the State Pension cost is scaled by the deterioration in the support ratio: 7.7 × (2.7 / 1.85) = 11.2% of GDP. Since the current State Pension bill of £138 billion is around 5% of GDP, 1% of GDP is approximately £27.6 billion; 11.2% of GDP therefore implies a bill of roughly £310 billion in today’s money. The exercise is intended only to illustrate the sensitivity of a pay-as-you-go pension system to adverse demographics.

[12] “Liberal Democrat Manifesto 2010”, https://www.markpack.org.uk/files/2015/01/Liberal-Democrat-manifesto-2010.pdf, p.19

[13] Cribb, Emmerson, Johnson and Karjalainen, “The future of the state pension”, IFS. https://ifs.org.uk/publications/future-state-pension (2023).

[14] Calculated using the following data sources: “Basic State Pension (Rate)”, Royal London, https://adviser.royallondon.com/technical-central/rates-and-factors/state-pension/basic-state-pension-rates/; “AWE, Whole Economy Level (£): Seasonally Adjusted Total Pay Excluding Arrears”, ONS, https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/earningsandworkinghours/timeseries/kab9/emp (April 2026); “CPI Index 00”, ONS, https://www.ons.gov.uk/economy/inflationandpriceindices/timeseries/d7bt/mm23 (April 2026).

[15] “Fiscal risks and sustainability – July 2025”, OBR, https://obr.uk/frs/fiscal-risks-and-sustainability-july-2025/ (2025).

[16] “UK’s pension triple lock to cost three times more”, BBC News, https://www.bbc.co.uk/news/articles/cy7nv3pdgr4o (2025).

[17] Heidi Karjalainen, “What are the effects of the ‘triple lock’ and how could it be reformed?”, IFS, https://ifs.org.uk/articles/what-are-effects-triple-lock-and-how-could-it-be-reformed#:~:text=Contents&text=The%20level%20of%20the%20state,with%20average%20earnings%20since%202011 (2025).

[18] Jun Saito, “Macroeconomic Slide Mechanism of the Japanese Pension System”, Japan Center for Economic Research, https://www.jcer.or.jp/english/macroeconomic-slide-mechanism-of-the-japanese-pension-system (2023).

[19] Raitano and Jessoula, “Changes in the pension debate under the new government in Italy”, ESPN Flash Report 2018/41, European Commission (2018).

[20] John Hooper and Phillip Inman, “Italy’s jobs minister fears for life as labour market shaken up”, The Guardian (2012), https://www.theguardian.com/world/2012/mar/23/italy-jobs-minister-elsa-fornero.

[21] Sawulski, Magda, Lewandowski, “Will the Polish pension system go bankrupt”, Instytut Badań Strukturalnych (2019) https://ibs.org.pl/app/uploads/2019/06/IBS_Policy_Paper_02_2019_en.pdf.

[22] “Pensions timebomb: why Europe’s social contract is becoming unsustainable”, The Guardian (2025), https://www.theguardian.com/money/2025/dec/29/pensions-timebomb-europe-social-contract-becoming-unsustainable.

[23] “State Pension age Review 2023”, Department for Work and Pensions (2023), https://www.gov.uk/government/publications/state-pension-age-review-2023-government-report/state-pension-age-review-2023.

[24] “UK launches review into raising state pension age”, Reuters (2025), https://www.reuters.com/world/uk/uk-launches-review-into-raising-state-pension-age-2025-07-21/#:~:text=LONDON%2C%20July%2021%20(Reuters),by%20workers%20towards%20their%20retirement.

[25] “Pensions at a Glance 2021”, OECD (2021), https://www.oecd.org/en/publications/pensions-at-a-glance-2021_ca401ebd-en/full-report/component-6.html.

[26] Browne and Smith, “The Lifespan Fund: Reforming the State Pension for a More Affordable, Flexible and Fair Future”, Tony Blair Institute, https://institute.global/insights/economic-prosperity/the-lifespan-fund-reforming-the-state-pension-for-a-more-affordable-flexible-and-fair-future (2026).

[27] Cribb, Henry, and Karjalainen, “How have pensioner incomes and poverty changed in recent years?”, IFS, https://ifs.org.uk/publications/how-have-pensioner-incomes-and-poverty-changed-recent-years (2024).

[28] “Income-related benefits: estimates of take-up: financial year ending 2024”, Department for Work and Pensions (2025), https://www.gov.uk/government/statistics/income-related-benefits-estimates-of-take-up-financial-year-ending-2024/income-related-benefits-estimates-of-take-up-financial-year-ending-2024.

[29] “DWP benefits statistics: August 2025”, Department for Work and Pensions, https://www.gov.uk/government/statistics/dwp-benefits-statistics-august-2025/dwp-benefits-statistics-august-2025 (2025).

[30] “Great Britain National Insurance Fund Account for the year ended 31 March 2025”, HMRC, https://www.gov.uk/government/publications/national-insurance-fund-accounts/great-britain-national-insurance-fund-account-for-the-year-ended-31-march-2024 (2025).

[31] “Paul Goldsmith on why using borrowed money to invest in the Super Fund is a bad idea, even if halting contributions would reduce the size of the fund by $20 billion over 10 years”, Interest, https://www.interest.co.nz/banking/107453/paul-goldsmith-why-using-borrowed-money-invest-super-fund-bad-idea-even-if-halting (2020).

[32] “Tackling Scotland’s population challenges”, Scottish Government, https://www.gov.scot/news/tackling-scotlands-population-challenges-1/ (2024).

[33] “Scotland’s birth rate falls to lowest level since 1855”, BBC News, https://www.bbc.co.uk/news/articles/c209en3zwyko (2025).

[34] Berrington, Kuang and Perelli-Harris, “Economic uncertainty and intentions to remain childless: Macro-economic worries or individual-level economic uncertainty”, Centre for Population Change, https://eprints.soton.ac.uk/497235/1/WP_109_Economic_uncertainty_and_intentions_to_remain_childless.pdf (2024).

[35] Calculated using Family Resources Survey microdata, please see appended methodology note for a full explanation. Calculation excludes Scotland, due to Scotland’s different income tax thresholds.

[36] “Free Childcare for Working Parents”, Gov.UK, https://www.gov.uk/free-childcare-if-working/check-youre-eligible.

[37] “Childcare Survey”, Coram, https://www.familyandchildcaretrust.org/sites/default/files/Childcare%20Survey%202024_5.pdf (2024).

[38] “Childcare and early years provider survey”, Department for Education, https://dera.ioe.ac.uk/id/eprint/41798/1/Childcare%20and%20early%20years%20provider%20survey%2C%20Reporting%20year%202025%20-%20Explore%20education%20statistics%20-%20GOV.UK.pdf, (2025).

[39] “Future rollout of new early years entitlements faces challenges”, National Audit Office, https://www.nao.org.uk/press-releases/future-rollout-of-new-early-years-entitlements-faces-challenges, (2024).

[40] “A focus on childminders”, Ofsted, https://www.gov.uk/government/publications/early-years-inspections-statistical-commentaries-2022-to-2023/a-focus-on-childminders (2023).

[41] “Main findings: childcare providers and inspections as at 31 August 2025”, Ofsted, https://www.gov.uk/government/statistics/childcare-providers-and-inspections-as-at-31-august-2025/main-findings-childcare-providers-and-inspections-as-at-31-august-2025, (2025).

[42] “Childcare shortage worsens as costs rise – report”, BBC News, https://www.bbc.co.uk/news/education-68580918 (2024).

[43] “Commentary: Changes in access to childcare in England”, ONS, https://www.gov.uk/government/publications/changes-to-access-to-childcare-in-england/commentary-changes-in-access-to-childcare-in-england (2024).

[44] https://www.progressive-policy.net/downloads/files/CPP_Growing-Pains-Report-_March-2023_SP.pdf

[45] https://www.pwc.co.uk/press-room/assets/impact-of-childcare-policy-in-the-uk.pdf

[46] Department for Education, “Childcare and early years survey of parents”, https://explore-education-statistics.service.gov.uk/find-statistics/childcare-and-early-years-survey-of-parents/2023 (2023).

[47] Franklin and Fogden, “Growing pains: the economic costs of a failing childcare system”, Centre for Progressive Policy, https://www.progressive-policy.net/downloads/files/CPP_Growing-Pains-Report-_March-2023_SP.pdf (2023).

[48] HM Revenue & Customs, “Looking after the grandchildren? Make sure it counts towards your State Pension”, GOV.UK, https://www.gov.uk/government/news/looking-after-the-grandchildren-make-sure-it-counts-towards-your-state-pension (2013).

[49] This is Money, “Grandparents can boost state pension by £6,000 just by looking after grandchildren”, https://www.thisismoney.co.uk/money/pensions/article-13568555/Grandparents-boost-state-pension-6-000-just-looking-grandchildren.html (2024).

[50] Department for Education, “Childcare and early years survey of parents”, https://explore-education-statistics.service.gov.uk/find-statistics/childcare-and-early-years-survey-of-parents/2023 (2023).

[51] Broome, Hale, and Slaughter, “An intergenerational audit for the UK: 2024”, Resolution Foundation, https://www.resolutionfoundation.org/app/uploads/2024/11/Intergenerationl-Audit-2024.pdf.

[52] Barslund and Schomaker, “Grandparental Childcare and Parent’s Labour Supply: Evidence from Europe”, Sozialer Fortschritt, Vol. 68, No. 4, https://www.jstor.org/stable/45174929 (2019).

[53] Broome, Hale and Slaughter, “An intergenerational audit for the UK: 2024”, Resolution Foundation, https://www.resolutionfoundation.org/app/uploads/2024/11/Intergenerationl-Audit-2024.pdf (2024).

[54] “Grandparents are saving families £96bn a year in equivalent childcare costs”, Sunlife, https://www.sunlife.co.uk/press-office/news/grandparents-childcare-salary/ (2023).

[55] Phoebe Arslanagić-Little, “A New Deal for Parents”, Onward, https://ukonward.com/wp-content/uploads/2024/08/NEW-DEAL-FOR-PARENTS-7-August-PM-PDF-1.pdf(2024).

[56] Childcare costs and hours are based on what a real family living in north London are paying, whose names have been changed.

If you value the work we do support us through a donation. Your contribution will help fund cutting edge research to make the country a better place.