The Anti-Social Contract

Renewing Our Social Contract

Phoebe Arslanagić-Little and Laurence Fredricks |

Published 23 June 2025

1200

627

1200

627

Phoebe Arslanagić-Little and Laurence Fredricks |

Published 23 June 2025

“Sometimes when I go to bed at night, I think that if I were a young man I would emigrate.”

Rt Hon James Callaghan to Cabinet, November 1974

****

A social contract seems like a logical, even natural, thing – until it isn’t. For time out of mind, it was widely accepted that if young people worked hard and did the right thing, Britain was a country where this would be rewarded with success. That success might be more or less dramatic, but its core elements – a good job, a decent home, the chance to raise a loving family – were commonly understood. They reflect very fundamental human needs.

The existence and importance of this social contract united both the political Left and Right. Whatever political tradition we flow from, there has been a broad confluence of agreement around this shared vision. Helpfully, throughout most of the twentieth century it was supplemented by gradually increasing material prosperity. Not for nothing did Mrs Thatcher celebrate the triumph of Marks and Spencer over Marx and Engels. Life transformed for the better for most Britons between the 1920s and the 1990s.

Yet today, our social contract is broken. Politicians may still deploy the rhetoric of an opportunity society, but the reality for many younger people is increasingly one of collapsing dreams. As this paper sets out, modern Britain is less “no country for old men” than “no country for young people”. Wage growth has been stagnant for years. Yet many crucial costs have soared: most notably, the cost of the average deposit for a home has tripled in real terms since 2000. Young people are trapped in expensive, often low-quality, rented houses deep into their twenties and thirties – or face the unattractive option of living as perma-teenagers with their parents. Meanwhile childcare is exorbitantly expensive. Unsurprisingly, our birth rate is collapsing, testified to eloquently but silently by closures of maternity wards and schools. This is a profoundly unhealthy place for any society to be.

In the face of this, the British state is running a kind of giant Ponzi scheme, with young people as the victims. An ageing society is catastrophically expensive for fewer people of working age to support. The OBR forecasts that by 2070, the state pension, adult social care and healthcare costs will account for almost half of government spending, compared to a third in 2020. Who seriously believes the triple lock can survive this kind of demographic change? On this trajectory, what are the odds on the state pension being affordable at all?

Immigration was long held out as the answer to economic and demographic sustainability, but it has proved no answer at all. The OBR’s analysis has exploded the myth that low-skilled immigration generates a net fiscal contribution – instead, the reverse is true. Meanwhile in recent years immigration has imposed huge new pressures on our housing stock, public services and social cohesion alike, further complicating existing problems and creating dangerous new fault lines.

Renewing our social contract is vital, and in all our interests. It is not simply a matter of fairness. It is about the viability of the nation. Without action, people will pay ever more in tax, but public services will decline and the national accounts still won’t add up. Without action, your parents’ wealth and the availability of the Bank of Mum and Dad will make more of a difference to your outcomes in life than anything you do. Without action, faith in mainstream politics and even democracy itself will increasingly be at risk.

The Left will call for redistribution, but you will never get ahead of the problem that way, and efforts to do so will kill economic growth. The only solution is to restore opportunity: to build the homes we need, to lower immigration to manageable numbers, to better support family formation and to open a rational conversation about a fair rebalancing of welfare entitlements. At its heart lies one key word: reciprocity.

This will not be easy. As the demographic squeeze grips tighter, so zero-sum positions become easier to adopt. But most of the threats to the social contract have been at least worsened, and in some instances entirely created, by public policy choices. As these were made, so they can be unmade. This launch paper begins the journey of setting out how this should be done.

Rt Hon Sir Simon Clarke

Director, Onward

Britain has become dangerously tilted towards older age groups in both its politics and its policymaking. The failure to confront the country’s changing demographic reality compromises not just intergenerational fairness, but threatens the medium to long-term sustainability of the state itself.

The ‘social contract’ is the implicit agreement between the British state and citizens, and between citizens themselves. It is a shared understanding that if people work hard, play by the rules, and contribute to society, they will be rewarded with opportunity and security. This shared understanding is reciprocal, not unilateral. It rests on principles of reciprocity, mutual obligation and consent and is not imposed by diktat.

For much of the post-war period, this social contract underpinned Britain’s political economy. Economic growth was strong, living standards rose from generation to generation, and the welfare state offered protection from hardship and at vulnerable times of life. There was a widely shared belief that hard work would lead to a better life, materially and in terms of dignity, agency, and the ability to build a future for oneself and one’s children.

But for younger generations, the link between contribution and reward has weakened. Home ownership, stable family life, and financial security – traditional milestones of adulthood – are becoming harder to attain, even for those in full-time work. At the same time, trust in institutions is falling, the tax burden on working people is rising (in some cases serving to penalise hard work and progress through high marginal tax rates), and important social infrastructure struggles to deliver. For many, the system no longer seems to work as promised: it demands more but delivers less.

These symptoms are the warning sirens of a breakdown in the social contract. That breakdown is driven by demographic change, economic stagnation, and a political class that is failing to adapt to new social realities. The working-age population is shrinking relative to the retired, yet is being asked to shoulder an ever-increasing fiscal burden.

At the same time, political incentives remain skewed towards older voters. This reinforces a system in which wealth and public spending increasingly flow to those in retirement, and away from those starting families, building businesses, or saving for the future, who are being asked to fund services that may no longer be available once they reach old age.

This paper makes the case for renewing the social contract for a new generation. It begins by diagnosing the material and institutional symptoms of breakdown and then explores the structural drivers of those symptoms. It then turns to the political challenge of how to communicate a vision of change that is both honest about trade-offs and capable of winning broad public support. Rebalancing between generations is essential. Not to play zero-sum games, or to divide society, but to preserve and strengthen it for future generations.

Identifying how the breakdown of the social contract manifests in people’s lives is key to understanding what is causing that breakdown. Below are detailed the major indicators that suggest the system is no longer working for too many people, especially working people.

That contribution is met with reward is key to working people’s sense that society works for them and is fair. Through taxes, the contributions made by working people fund key social infrastructure that all rely on, or expect to rely on in the future, from healthcare that is free at the point of use to the State Pension. In exchange for these contributions, working people expect to be able to build a good life for themselves. They also expect that the social infrastructure they have helped to fund will be there when they themselves need it, particularly in old age.

This link between contribution and reward is breaking down. Working people are being asked to increase their contributions, but as the demands upon them increase key elements of a good and stable life drift out of their grasp. Even the likelihood that key elements of the social infrastructure they have helped to fund will one day be there for them is decreasing.

This breakdown is visible across several important indicators. It is more difficult to buy a house or start a family. Inherited wealth is an increasingly important determinant of their life outcomes, trumping the returns on hard work. Higher taxes are making work itself less attractive to younger generations. And even for those in work, levels of debt are increasing.

The housing crisis means that fewer people are able to buy a home and those that can are being forced to wait longer and longer to do so. Average property values for first time buyers have reached 6.6 times the average UK salary, meaning that even those in full-time employment have years of saving ahead of them to get into a position to buy a home.1

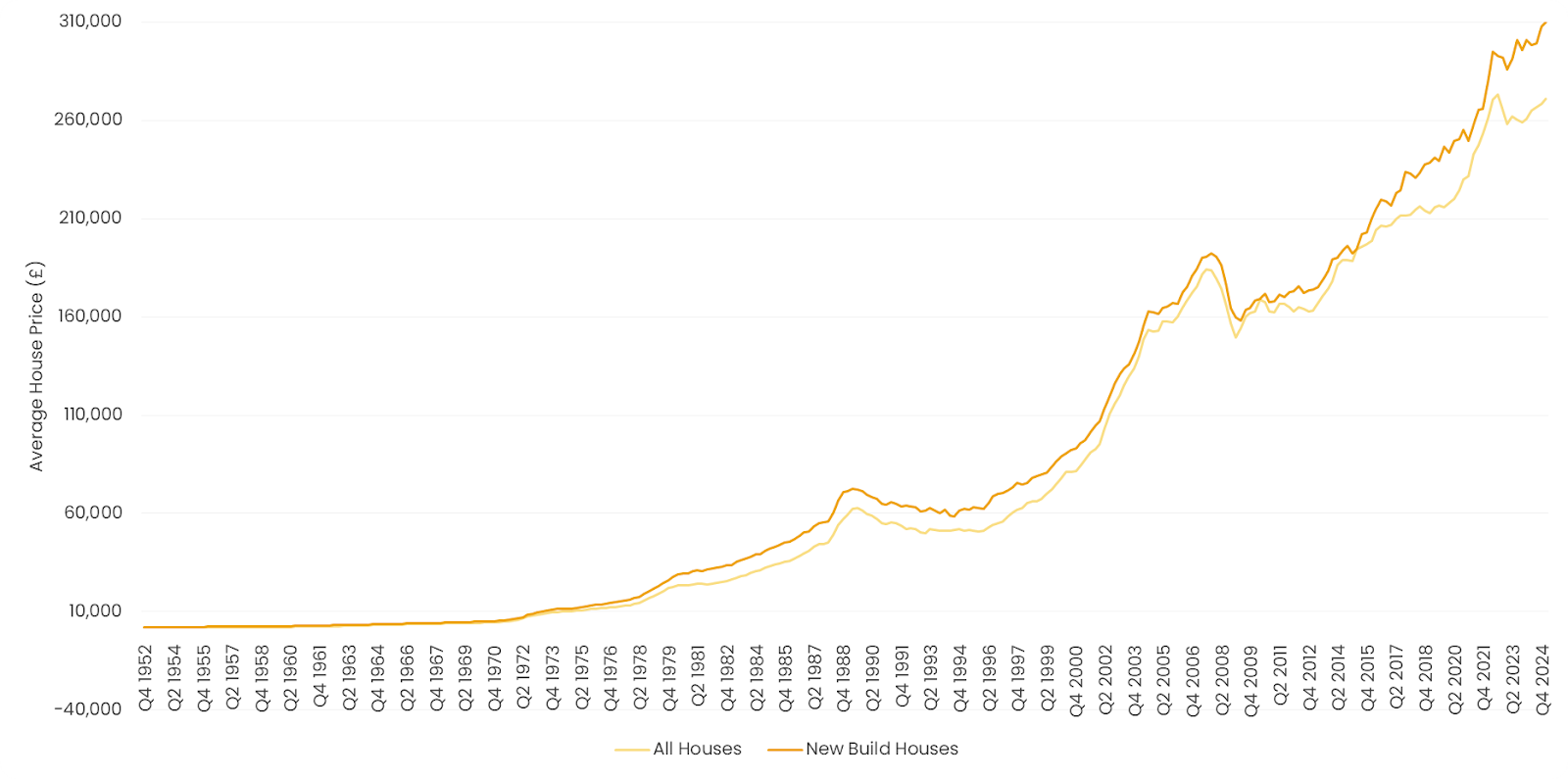

Figure 1: Average UK house prices have rapidly increased and new build homes have become comparatively more expensive.

Source: Nationwide2

In 2025, very different financial demands are made of a working person in their late twenties or early thirties looking to buy their first home than those twenty years ago. In 2000, the average deposit for a first home was £9,865 (£18,349.50 in real terms).3 Today, it is over £60,000.4 As a result, first time buyers are getting older. The average age of a first time buyer hit 33 in 2024, up from 29 in 2000 and 27 in 1980.5

This means today’s buyers will still be paying off their mortgages much later in life, potentially delaying retirement in order to be able to do so. But even as the average age of first time buyers increases, mortgage terms are also increasing with ultra-long mortgages becoming more popular as a way of bringing down the cost of monthly payments.6 In 2015, the average mortgage term for a first time buyer was 28 years, but today it is 31 years.7 Ultimately, accruing interest means that these extended mortgage deals are more expensive for buyers.

Renters are also being squeezed. The average monthly cost of renting a room is £744 in the UK as a whole.8 Rents are highest in Greater London, where the average cost of renting a room is nearly £1000 and cheapest in Yorkshire and Humberside at £557.9 Prices have risen considerably over the past decade. In 2015, renting an entire one bedroom flat in Greater London cost £1,155, only around £155 more a month than a room does today.10 Renting a room in Huddersfield, Yorkshire in 2015 cost an average of only £350 a month.11

High rents and expensive deposits work together to make it very difficult for younger people to save enough to buy a home, even when in fulltime, well paid work. The average time to save for a mortgage deposit has hit 7 years and the average worker saves just 1% of their income.12 Furthermore, the 70% of first time home buyers who buy without assistance from the so-called Bank of Mum and Dad, are likely to take longer to save for a deposit.13 Today, only 10.4% of people aged 20 to 44 have the level of income and savings that would allow them to buy their first home.14

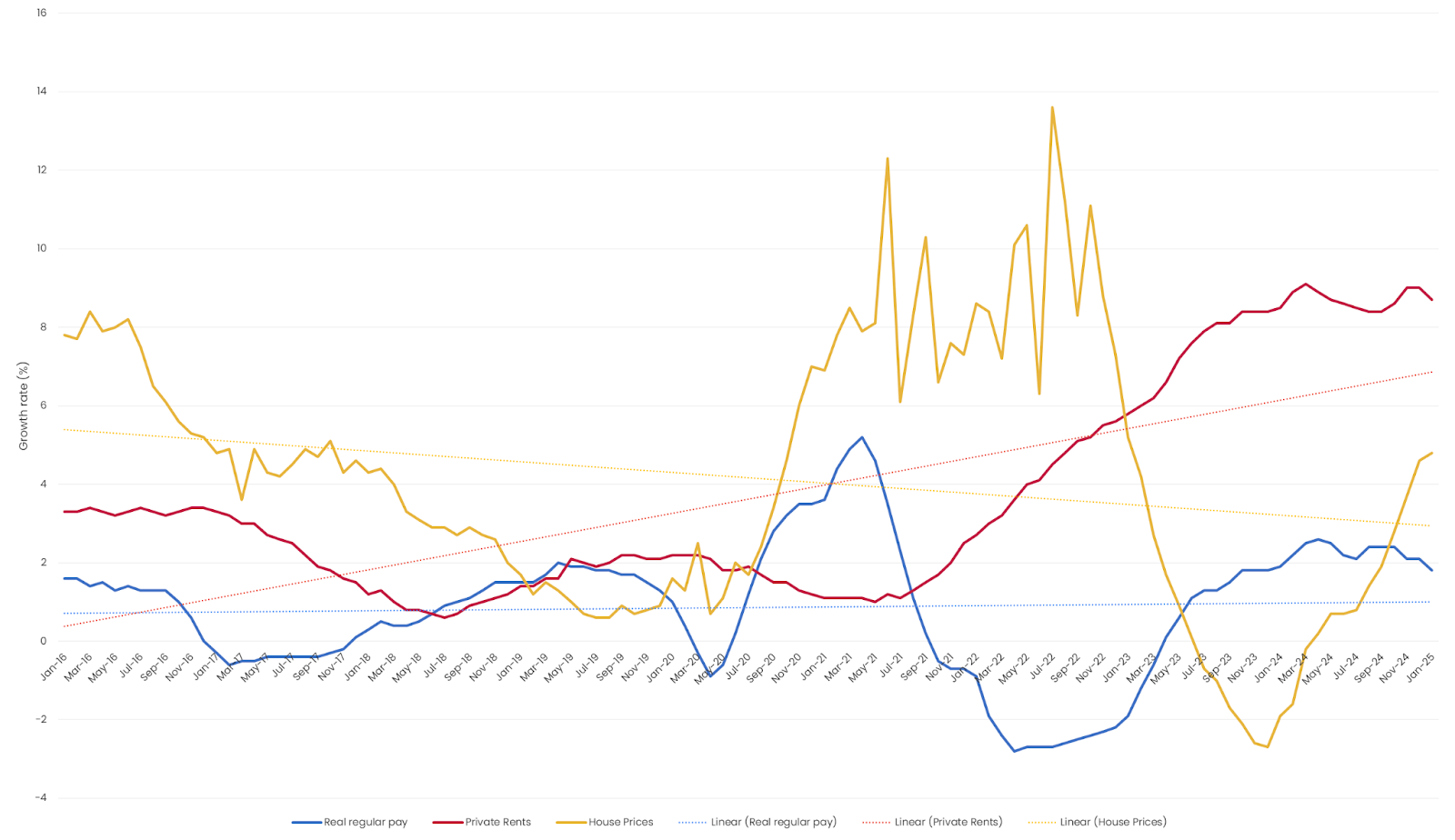

Figure 2: Young people are caught in an affordability trap. House price inflation has cooled, but private rent inflation has skyrocketed amidst stagnating wage growth.

This means that younger people are forced to make difficult financial decisions in order to build up the savings necessary to put a deposit down on a first home. Pension contributions are often among the first sacrifices made by these hard-pressed savers, putting the old-age financial security of an entire generation at risk. Among recent and prospective homeowners, 15% have paused, reduced, stopped, or never started saving into a pension.17 This figure rises to 19% among first-time buyers, as younger generations make the trade off between buying somewhere to live and preparing for retirement.18

UK women are having fewer children than they want to have. British women of childbearing age say they want 2.35 children on average, but England and Wales’ birth rate is 1.44 children per woman and falling.19 20 In Scotland, the birth rate has fallen to 1.28, closing in on ultra-low fertility nations like Japan.21

In part, the UK’s falling fertility rate is the result of people waiting longer to start their families, with the average age of first time motherhood rising to 29.1 in 2020, up from 26.5 in 2000.22 But developing alongside the increase in delayed parenthood is a rise in childlessness. 18% of women born in 1975 are childless, up from 13% of those in their mother’s generation.23 Childlessness is increasing markedly in younger generations also. Of women born in 1993, the majority (56.5%) were childless by the age of 30.24 While many of these women will go on to have children, their chances of remaining childless are higher, even as the majority of young women continue to want two children or more.

Figure 3: Women in England and Wales had over 300,000 births fewer than desired in 2023.

Source: ONS, Onward analysis25

Tellingly, childlessness is not being felt evenly across British society. The UK has a widening ‘parent gap’ between rich and poor, with wealthier people increasingly more likely than poorer people to ever become parents.26 In short, factors like sky-high rents and childcare costs mean that many are less likely to ever be in a position to become a mum or dad, perhaps particularly in the era of intensive parenting as society’s sense of the resources necessary to raise a child increase. In 2023, 41% of Brits who were unsure about having children said they would need to become “less economically vulnerable” to do so.27

For those who are parents, policy choices make it more difficult to bring up children or to expand their families. Parents are more likely than those not raising children to be struggling financially and be behind on mortgage payments and other bills.28 Children are especially costly to parents in early childhood, reducing parents’ ability to work and because of childcare costs. Yet not only do parents pay the same tax as non-parents, with no recognition of the cost of children in the UK’s tax system, but the UK has several policies which directly make parents’ lives more difficult. This includes the tapered means-testing of Child Benefit starting at a salary of £60,000 and the two child benefit cap, which means families can only receive the child element of Universal Credit, or the legacy benefit Child Tax Credit, for a maximum of two children.

Poor pay progression post the 2007 financial crisis, coupled with the cost of living crisis and inflation, mean that working people are accruing higher levels of debt. This includes problem debt, with an increasing number of people struggling to make repayments.

As goods become more expensive, consumers are relying more heavily on credit, with credit card debt rising by nearly 10% in 2023.29 The debt charity StepChange has not only seen an increase in those seeking their help in the past few years, but specifically an increase in those who are in full-time employment but still have problem debt: nearly 3 million people are in full-time work yet unable to afford debt repayments.30

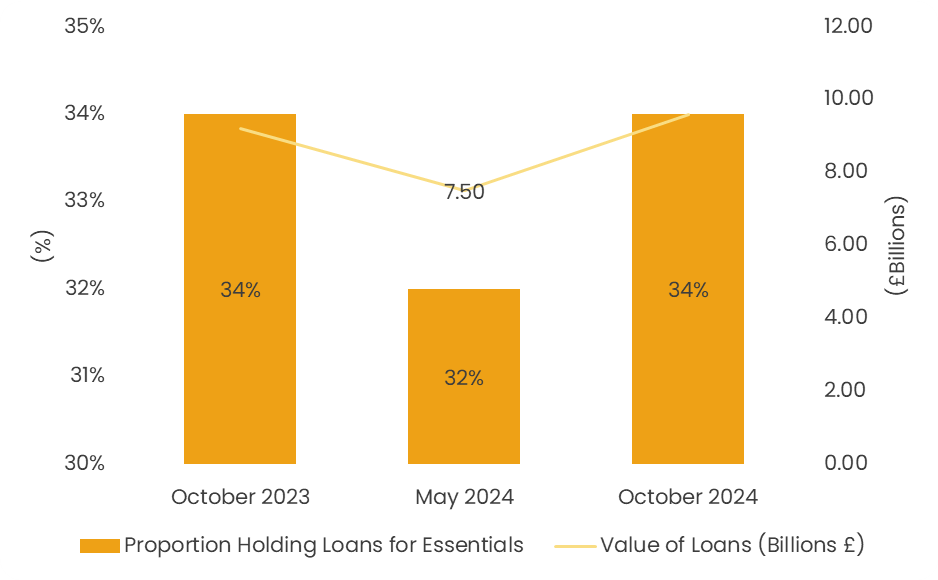

Figure 4: An increasing share of low income households are having to take out loans to pay for essentials and those loans are of an increasing value.

Source: Joseph Rowntree Foundation31

An increasing number of working people are also burdened with student debt. Total outstanding student debt owed to the government was £250 billion at the end of 2024. With university tuition fees rising again, the average amount of student debt owed by a graduate leaving university in 2025 is £45,600.32 In 1999-2000, UK university students left university with approximately £2,500 in student debt.33

The student loan system has also recently become less generous in the wake of reforms made in 2022, particularly for lower to middle earning graduates. Pre-2022, student loans essentially worked as a graduate tax, but post-2022, the majority of students will pay off their loans in full.

One part of these reforms has been to lower the salary threshold for making repayments on student loans to £25,000.34 This means that a graduate earning the minimum wage and working full-time will be making payments on their loan.

The mortgage debt that people owe has also risen to very high levels, in large part because of the rise in house prices. By the end of 2024, the total outstanding value of all residential mortgage debt was £1,678.2 billion.35

Including mortgage and student debt, the above factors combine to mean that total UK household debt passed £2 trillion in 2023; enough to fund the UK’s spending on defence for over thirty years.36

As the link between hard work and reward weakens across key areas of life including homeownership, family formation and financial security, a broader sense of disillusionment with the way that Britain works – or does not work – is also taking hold.

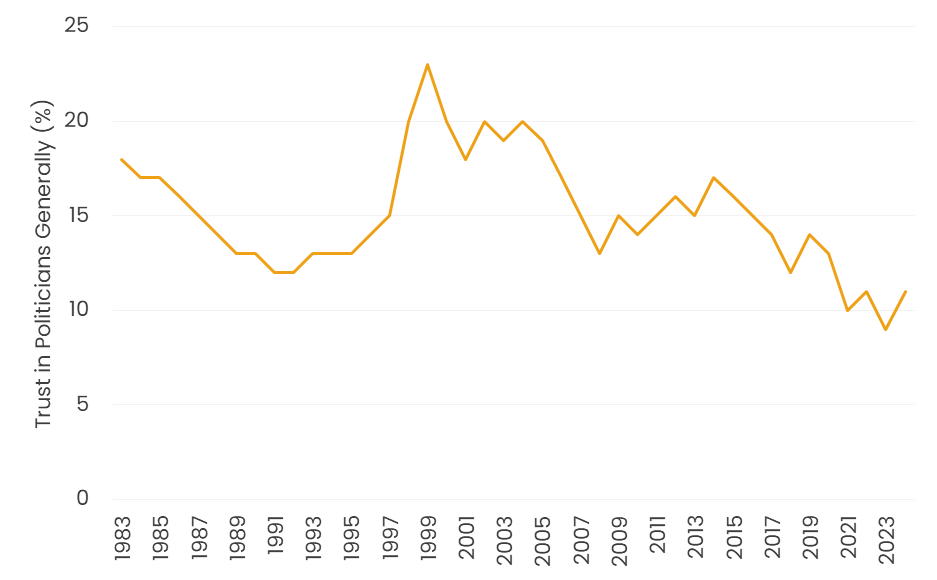

Public faith in institutions to listen, respond, and deliver is declining. This is reducing the legitimacy of the political system and driving voters to support populist alternatives like Reform UK, with trust in politicians collapsing to a 40 year low in 2023 and recovering only modestly in 2024.37 The loss of public faith in institutions can be seen in declining trust in the government, the political system as a whole, and also important public bodies like the police.

Figure 5: Trust in UK politicians has collapsed.

Source: IPSOS38

The public’s trust in the government’s ability to deliver is falling, alongside a loss of faith in how the UK is governed. Only 14% of Britons trust the government ‘most of the time’ or ‘always’.39 79% say the system of governing Britain could be improved.40 There is also a generational trust gap opening up, with younger people less likely to say they trust politicians. 2% of 25-34 year-olds and 8% of 18-24 year-olds say they trust politicians to tell the truth, compared to 13% of those aged 65 and over.41

There is a corresponding loss of faith in how the UK is governed. Confidence in the traditional political parties is waning. Nearly a third of the public (31%) say they do not feel represented by any of the UK’s main parties.42 Falling confidence in traditional parties has coincided with the ascent of populist alternative party Reform. In the 2024 General Election, Reform secured 14% of the vote and sent five MPs to Parliament. In the May 2025 local elections, Reform won the plurality of the vote (31%) and the majority of seats.43

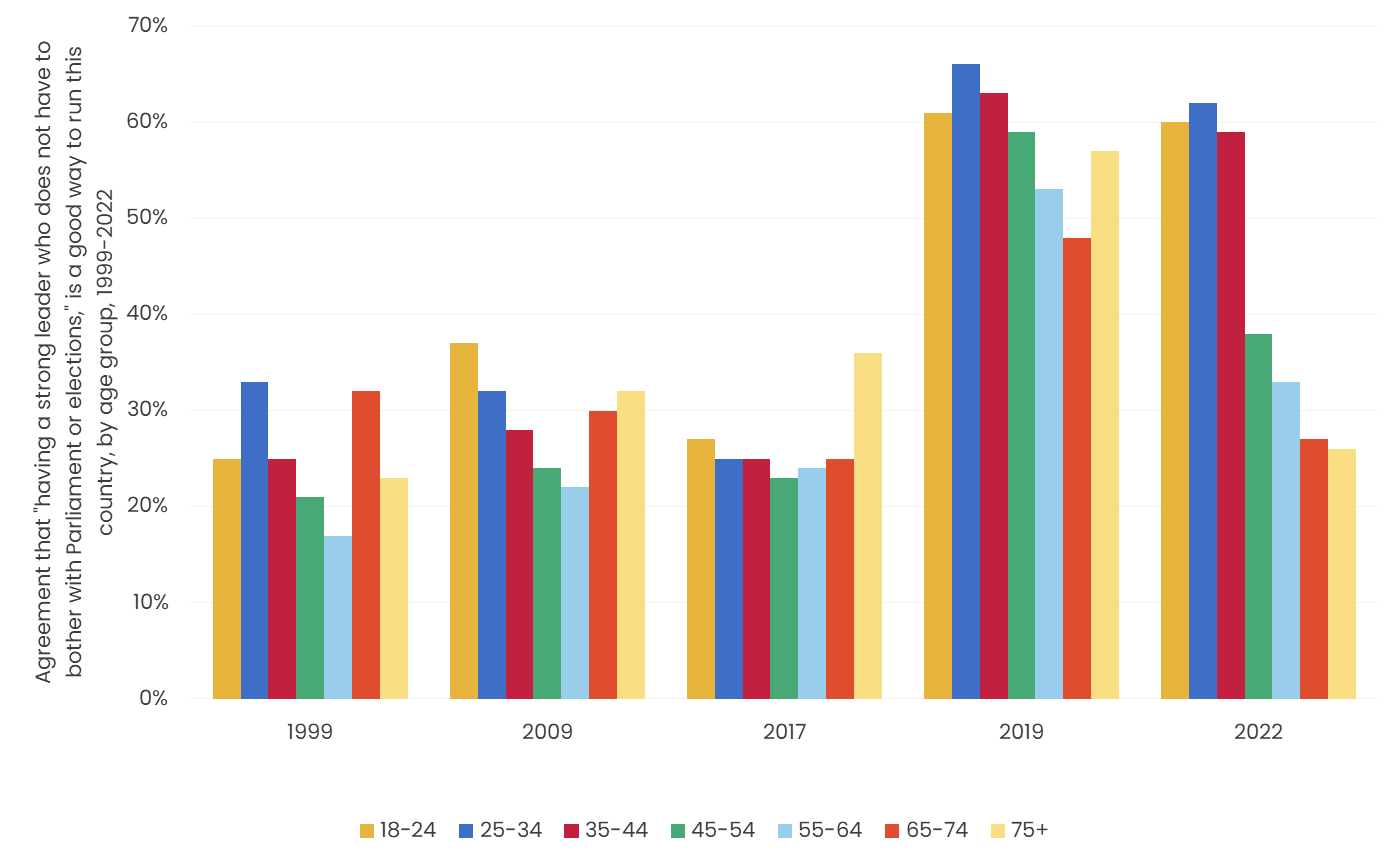

Figure 6: There is growing support for authoritarian alternatives of governance, particularly amongst the young.

Source: Onward44

Again, there is evidence that this loss of faith in our political system is concentrated among younger people. 2022 Onward research shows rising support for authoritarian governance among young people.45 61% of 18-34s agreed that “having a strong leader who does not have to bother with parliament and elections would be a good way of governing this country” and 46% agreed that “having the army rule would be a good way of governing this country”. In comparison, only 29% and 13% for over-55s agreed with these statements, respectively. A quarter (26%) of 18-34s thought that democracy is a bad way of governing the UK, while only 8% of those aged over 55 did.

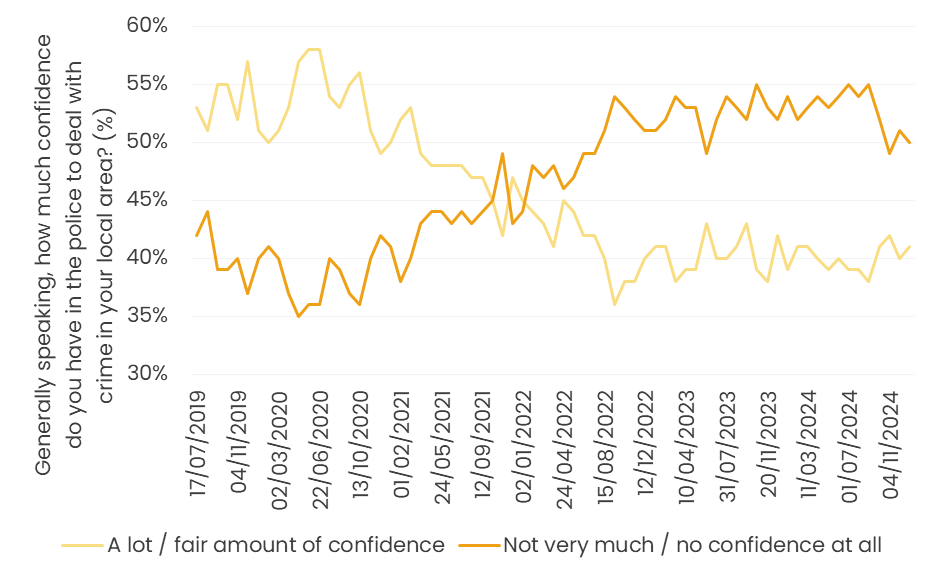

Figure 7: Falling confidence in the state is not limited to the Government, but also institutions such as the police.

Source: YouGov46

Alongside declining faith in how we are governed, there is falling public trust in important public services and institutions, including the police and their ability to maintain law and order. Nearly 80% of people in England and Wales believe that crime is rising and public faith in the police has fallen along with an increase in antisocial behaviour and highly visible types of crime, such as shop lifting, vandalism and fare dodging.47

Around 70% of the public think the police have effectively “given up” on tackling low-level crimes of this kind.48 Over a third of the public say they would not bother reporting a crime, believing doing so to be pointless as the police would do nothing about it.49 52% of the public say they have little to no faith in the police to carry out their core duty of tackling crime.50 The increase in highly visible crimes and antisocial behaviour coupled with the public’s sense of a withdrawal by the police fuels an atmosphere of impunity among both offenders and members of the public.

The symptoms identified above, including economic strain, diminished life prospects and disillusionment with how Britain is governed, are the warning indicators of deeper, structural strains on the social contract. This section identifies and describes those forces and pressures.

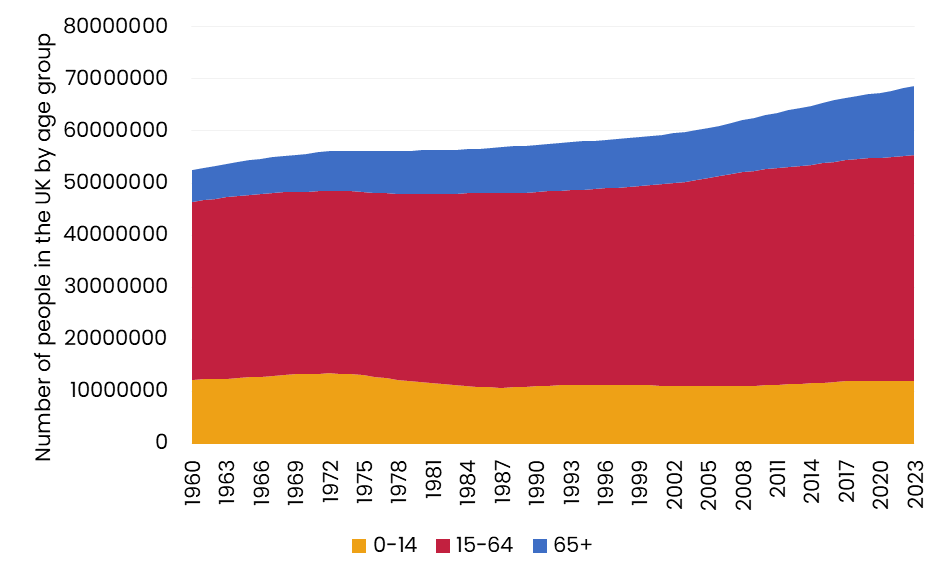

The UK has an ageing population, caused by longer life expectancies and falling birth rates. This changing population pyramid is eating away at the social contract by increasing financial pressure on the state, driving desperate governments to seek to alleviate that immense economic strain by increasing their demands upon working-age people and increasing immigration.

In 1950, the UK had an old-age dependency ratio of 16.2%. That means that for every 100 working-age people, there were 16 people aged over 65. Today, that has nearly doubled to 30 people aged 65 for every 100 working-age people.51 The ONS predicts that the UK’s population will increase by over 13 million to 81.7 million by 2070, and it expects two-thirds of the people comprising that increase to be aged over 65, giving us a working-age dependency ratio of 47%.52 This represents a hugely increasing burden on the shoulders of working people.

Figure 8: The UK is an ageing society.

Source: Our World in Data53

The ageing population is the result of two factors: increasing life expectancy and falling birth rates. As detailed above in section X.X on the birth gap, British people are having fewer children in a trend that is picking up pace. Between 2000 and 2023, the proportion of people aged over 65 increased by 41%. But the proportion of people aged under 15 in the UK’s population increased by 7%.54 Already, the UK is a nation of fewer and fewer children. All over the country, classrooms are emptying out and schools are closing down. London’s primary schools are emptying particularly rapidly: the capital saw a 20% decrease in its birth rate between 2012 and 2021.

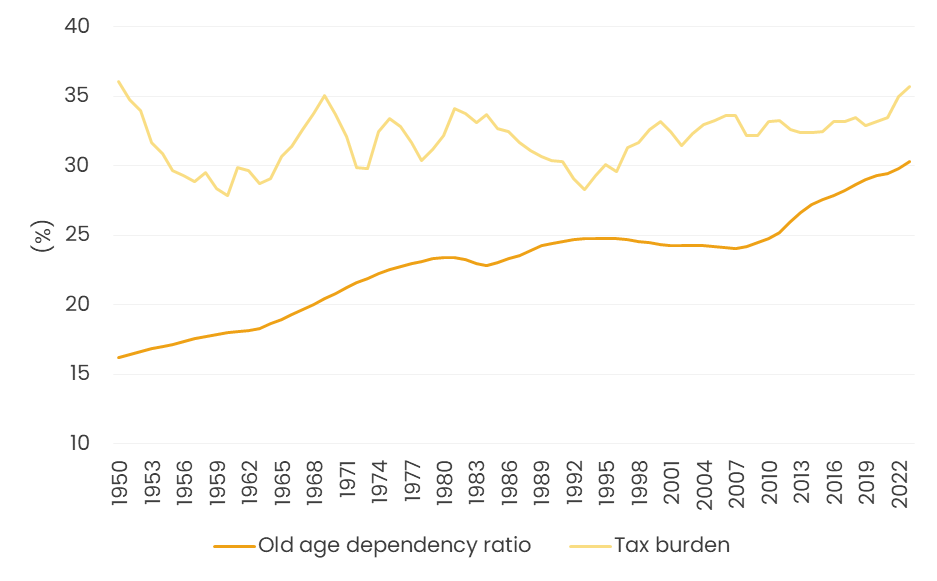

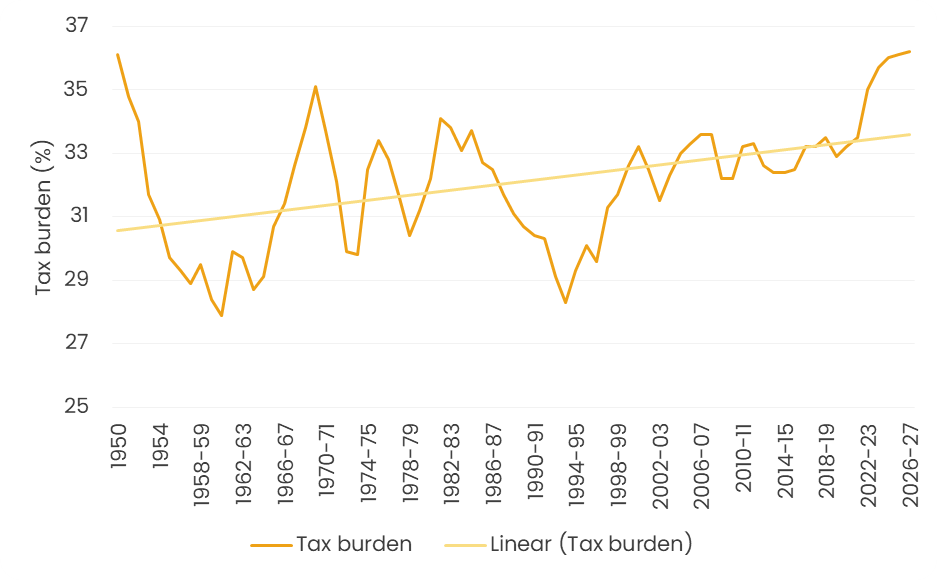

Figure 9: The tax burden is rising to an all time high whilst the gap between the old age dependency ratio and tax burden has been narrowing in recent years.

Sources: Our World In Data, Tax Payers Alliance5556

The situation poses a significant challenge for policymakers because an older population is an inherently very costly one. Public spending per individual soars with age and an older population exerts great pressure on public services. The OBR projects that State Pension, adult social care, and healthcare costs will account for nearly 50% of UK government spending in 2070, up from 35% in 2020.57

The strain is particularly visible in local authorities which already have a higher proportion of older people.58 In 2023, Hampshire County Council’s spending on social care made up 83% of its budget, up from 53% in 2011.59 As the people of the baby boom generation – comprising a fifth of Britain’s population – continue to retire and reach old age, this problem will become markedly more severe in the next decade.

Yet, as this demand on the public purse intensifies, its income through tax revenue will diminish because low birth rates mean the working-age population shrinks. This not only harms productivity and economic growth, but severely curtails our ability to care for this older population and to provide entitlements like State Pension.

Indeed rising costs coupled with dwindling revenue may simply mean that the state finds it impossible to maintain provision of key entitlements for citizens, such as healthcare that is free at the point of use, a State Pension, and government-funded care homes. This means that the working-age population of today are paying high taxes to fund services that may simply not exist by the time they are old enough to need them.

If the status quo is to be maintained, there are three main options available to the government, in addition to ever increasing national debt. One, taxes can be increased to bolster revenue to the public purse, even as the working-age population shrinks. Two, higher levels of immigration can be sought to boost the working-age population and ameliorate the old-age dependency ratio. And three, the government can increase the UK’s birth rate, although this third option will take time to have an impact.

The first two of these options are already pursued by policymakers, but are unsustainable, piling yet more pressure onto the social contract.

Already, the tax burden on working people is increasing. Between 2010 and 2019, tax revenue as a share of national income stayed at 33%. But as of 2024, it has increased to 36%, the highest tax burden since 1948.60 Much of this increase in taxes has occurred through fiscal drag: personal tax thresholds have been frozen since 2021, meaning that more and more taxpayers are being moved into higher tax brackets.

Figure 10: The tax burden is at a high.

Source: Tax Payers Alliance61

In addition to fiscal drag operating as a tax rise by stealth, many working people are also facing very high marginal tax rates. The marginal tax rate refers to the percentage of tax that applies to the last portion of income earned. Very high marginal tax rates are an artefact of poorly designed policies, including: the tapered means-testing of Child Benefit; the withdrawal of the free childcare hours entitlement for those earning over £100,000; the removal of the personal tax-free allowance for those earning over £100,000; and the student loan system.

Marginal tax rates mean that a parent in London with two children under five is actually better off earning £99,999 than £149,000, strongly disincentivising such an individual to seek progression and a higher pay.62 Indeed, there is strong evidence that high marginal tax rates are acting to disincentivise work and progress, with a clear and increasing trend of bunching of salaries around tax thresholds.63

Together, a higher tax burden and high marginal tax rates are eroding the link between work and reward. When demands upon earners increase, even as their hard work and success lead only to marginal increases in take-home pay, or actively leaves them worse off, the motivation to continue contributing into the system diminishes, to everyone’s disadvantage.

Nearly two decades of low productivity in the wake of the 2007 financial crisis is straining the UK’s social contract by opening up extremely wide regional disparities in opportunities and wealth, and by creating an economy in which the returns for hard work are diminished.

Between 1993 and 2008, the UK’s annual average growth was around 2%, but has hovered at 0.5% since then.64 This economic stagnation has been unevenly distributed across the country, with long-term regional disparities leaving many communities feeling economically excluded. In the 1980s the productivity of London was approximately 128% that of the UK average. But today it is as high as 170%.65 When London is removed from the equation, the UK is less wealthy per capita than Mississippi, America’s poorest state.

The British people are aware that some areas are doing considerably better than others, and that wealth and opportunity are concentrated in some regions. Nearly half of Britons say politicians focus more on some areas than others (48%) and that job opportunities are unevenly distributed (47%).66 This regional disparity and awareness of it contributes to a sense that the system is not working well for everyone and is unfair.

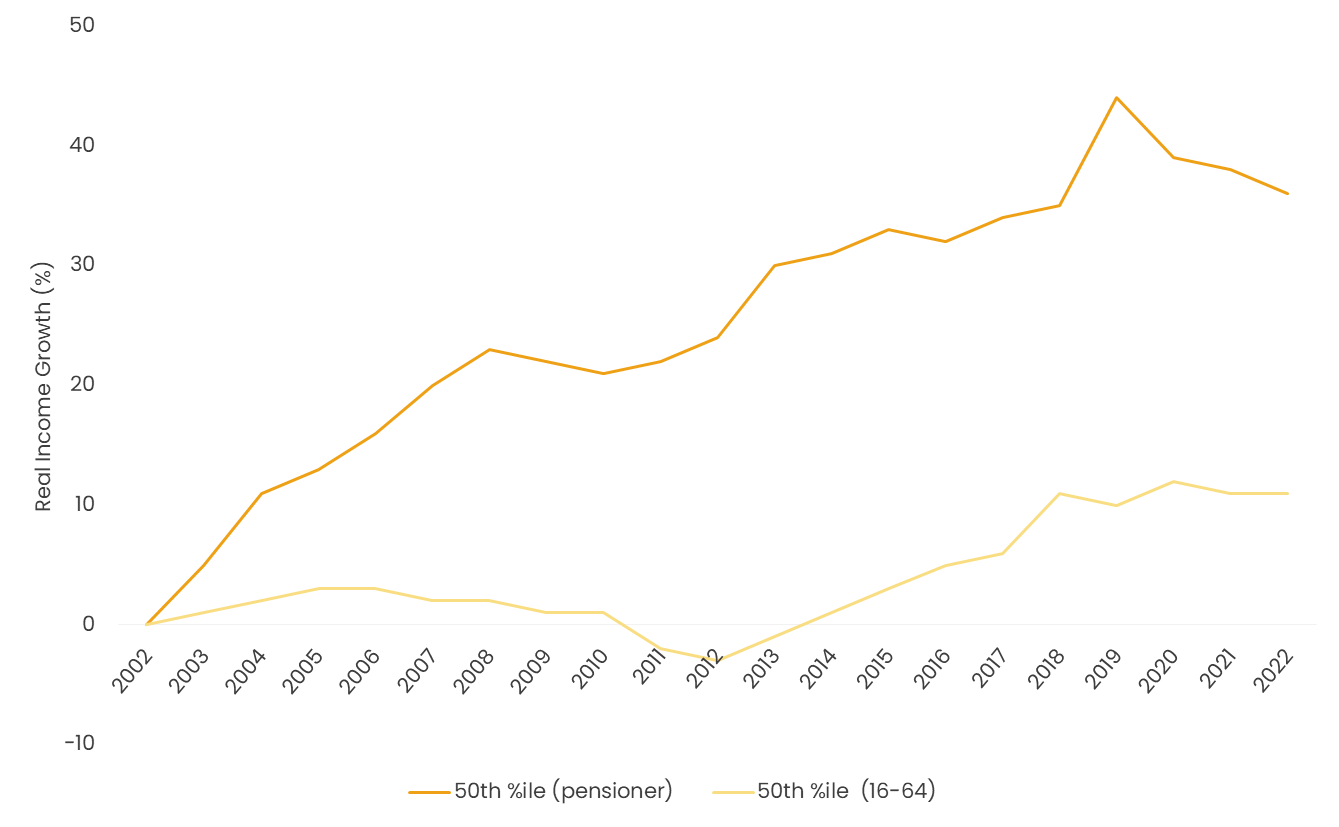

Another major consequence of the UK’s record of low growth and productivity is stagnant wage growth. If median incomes had continued to grow according to the pre-2007 financial crash trends, they would have grown 30% between 2010 and 2023.67 Instead, they grew 6%.68 Median household disposable income crawled up by just 7% between 2008 and 2023.69 This is in stark contrast with the 15 years before the 2007 crash, when median household disposable income increased by 41%.70

Figure 11: Median real income divergence between pensioners and the working age population has been stark and is protected by state transfers.

Source: Institute for Fiscal Studies71

Yet even as earned income has been stagnant, asset prices have gone up. This means that wealth has grown rapidly in comparison with earnings. This has increased intergenerational inequality and made inheritance and family wealth a greater determinant of life outcomes. Even as the economy has reflected in poor wage growth for the working age population, pensioners have seen significant real improvements in their incomes at the same time.

In recent years immigration has spiralled out of control. In 2022, 2023 and 2024 respectively, gross migration to the UK exceeded one million every year.72 This was despite the British people repeatedly voting to bring numbers of arrivals down. Immigration of this volume has strained our social contract by: reducing trust in the government’s ability to deliver or to respond to clear signals from the public; increasing pressure on infrastructure and public finances; and negatively affecting community cohesion.

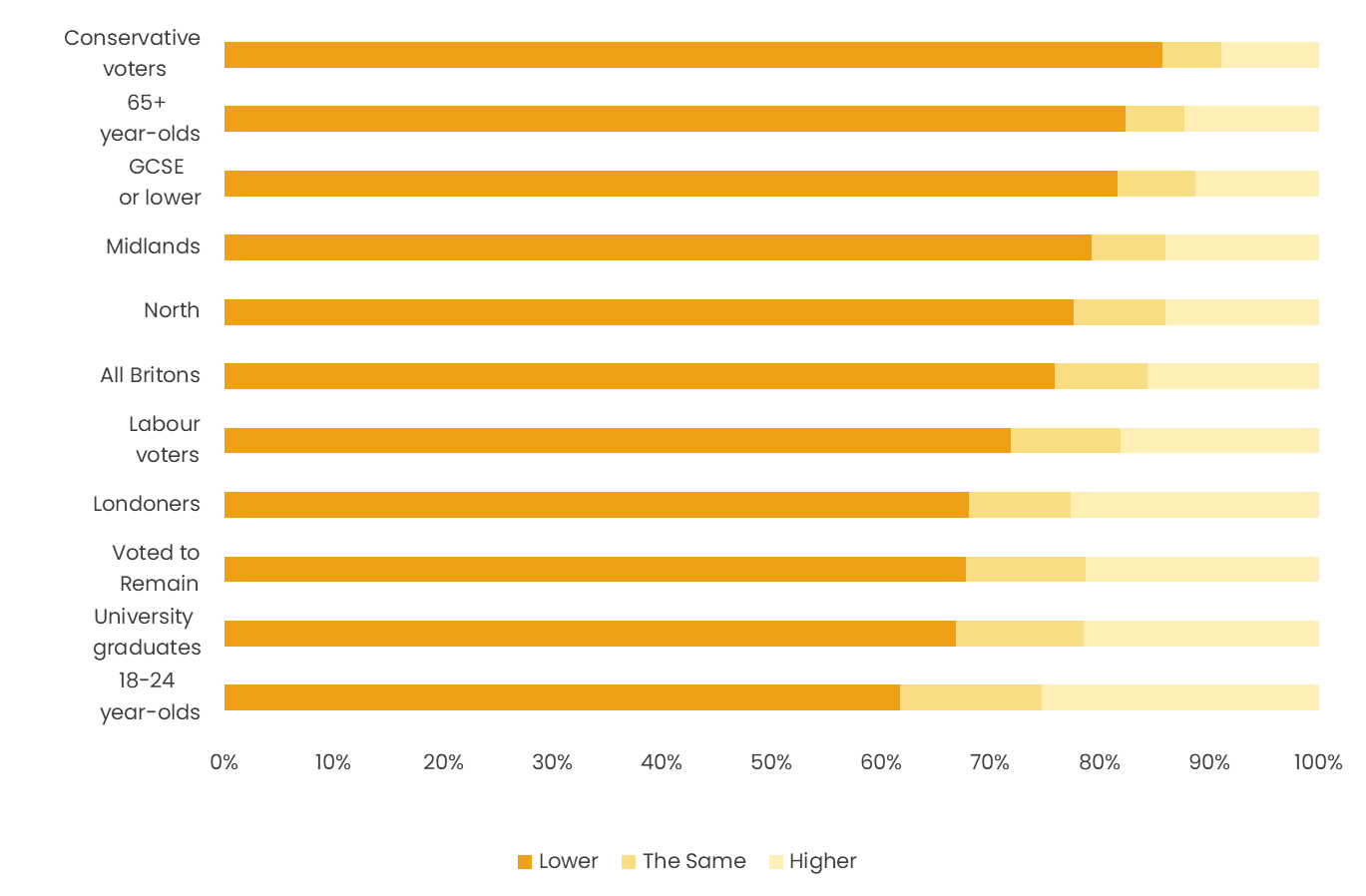

2024 Onward research found that the public underestimate the amount of immigration to the UK, with the average estimate 70,000, an estimation of some 17 times fewer people than the actual number.73 But even though the majority of British people very considerably underestimate net migration to the UK, they still believe it should be much lower. This is even the case among groups more likely to be more pro-immigration, including those aged 18-24 and Remain voters.

Figure 12: Voters across all key segments desire lower immigration.

Source: Onward74

Polling from 2023 shows that 52% of British people say immigration should be reduced, in comparison with only 14% who favour an increase, and the public have repeatedly voted to reduce the number of immigrants arriving in the UK.75 33% of those who voted in favour of Brexit in the 2016 Referendum said that restoring control over immigration was their main reason for voting to leave the EU.76

Despite these clear signals from the public, immigration has increased under successive Labour and Conservative governments for more than twenty years. Since 2010, six prime ministers have each promised to bring down the number of people arriving into the UK, and all have failed.

A very similar story has played out with illegal immigration. The number of people who have been detected arriving in the UK without authorisation has sharply increased since 2019, driven by an increase in the number of people arriving via small boats across the Channel. In 2024, 43,630 irregular arrivals, an increase of 19% compared from 2023.77 84% of irregular arrivals in 2024 were people who came to the UK via small boats. Since 2020, successive governments have promised to crack down on small boat arrivals and have failed to do so.

In addition to wearing away public trust in elected politicians’ ability to deliver key pledges and promises they have run on, the volume of both legal and illegal immigration received by the UK is putting pressure on infrastructure and public finances and services.

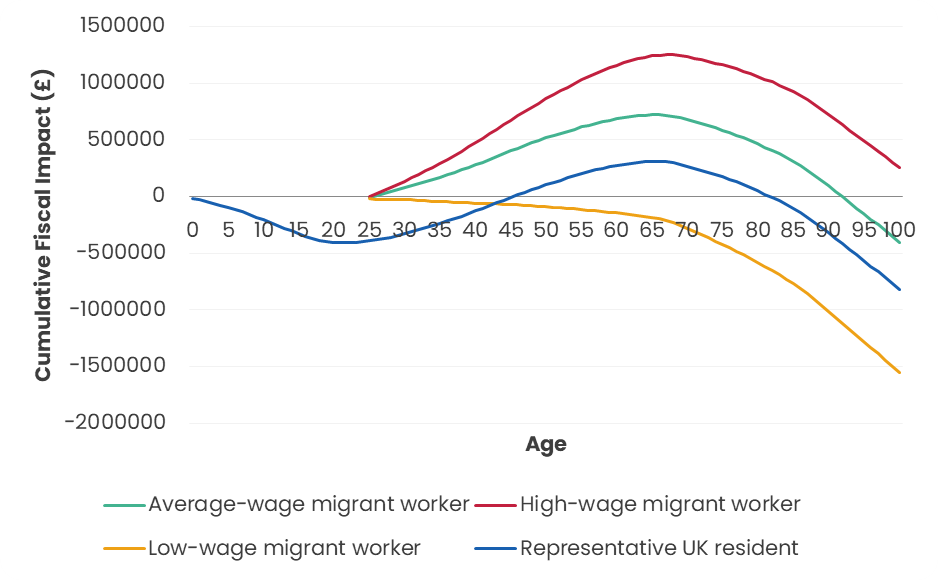

Figure 13: Low wage migrant workers are negative fiscal contributors.

Source: Migration Observatory78

Analysis shows that many of the recent arrivals to the UK will not be net fiscal contributors to the UK, but instead net recipients of government money.79 Out of the UK’s two million non-EU arrivals between 2019 and 2024, only 15% explicitly came to work, making it less likely that they will be net contributors.

One reason for this is because once an immigrant has lived in the UK for five years, they are eligible to apply for Indefinite Leave to Remain (ILR). A successful application for ILR entitles a non-citizen immigrant to many of the same benefits that citizens enjoy, including a State Pension, and access to Universal Credit and social housing.80 Based on historical patterns of ILR applications, analysis suggests that the ultimate long-term cost to British taxpayers will be £234 billion or more for providing these entitlements to immigrants who arrived in the UK between 2021 and 2024.81 It is also important to recall that even before an immigrant is granted or applies for Indefinite Leave to Remain, they are still entitled to use state-funded services like the NHS.

Many of those who arrive in the UK irregularly, principally via small boats, claim asylum and must be housed by the government while their claims are processed. Temporarily housing refugees and asylum seekers is proving extremely costly. In 2023, hotel accommodation for migrants – not including the cost of housing migrants in private rented accommodation – cost the tax payer £8 million per day.82 These costs have been driven up by the increase in the number of people arriving in the UK via small boat and the subsequent backlog in processing asylum claims.83 Over the next decade, the cost of accommodation for asylum seekers is projected to reach £15 billion.84

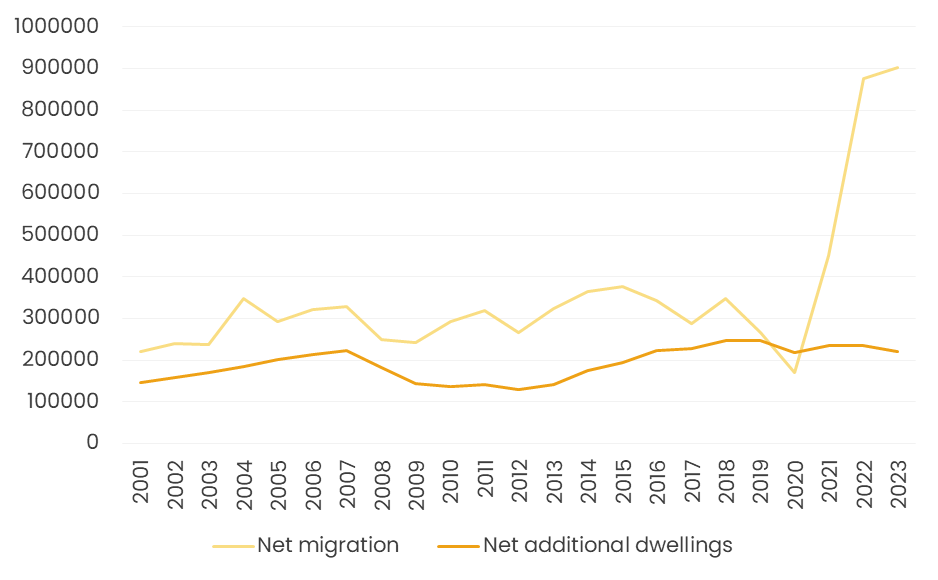

The exceptionally high levels of immigration to the UK in recent years is also contributing to the housing crisis, by causing a significant surge in demand in a housing market where there is already a serious shortage of homes to rent and buy. This increase in demand, with no corresponding increase in the supply of homes, means a more intense competition for properties and higher prices.

Figure 14. Net housing is below target and shortages are exacerbated by the additional pressures of net immigration.

Sources: MHCLG, Migration Observatory8586

Analysis shows that in 2022 alone, immigration to the UK would have meant an additional net 450,000 people entering the rental market.87 This effect will be concentrated in larger cities, also where housing shortages are most acute – 67% of privately rented households in London are headed by someone who was not born in the UK.88

The social contract does not solely consist of economic exchange or legal obligations, but also rests on shared norms and trust. In recent decades, changes have weakened these norms or at least made us question the extent to which they still exist. Onward’s Social Fabric Programme has identified these trends across the UK and created its Social Fabric Index to map them.89 These shifts, though less tangible than fiscal or demographic ones, nonetheless interact with the assumptions and obligations that form the social contract, and may be acting to undermine it.

The above section explains how very high levels of immigration to the UK has eroded public trust in politicians’ ability to deliver and put pressure on public finances and infrastructure. But the rapid influx of people into Britain over the past few years has also had a great impact on communities, with many areas left to grapple with changes in community identity.

Figure 15: England and Wales have experienced rapid demographic change by share of the population in the last two decades, with the growth in absolute number of non-UK born residents between 2011 and 2021 pinpointed.

Source: ONS, Onward Analysis90

Between 2001 and 2021, the number of immigrants as a share of the population doubled from 8.9% of England and Wales, to 16.8%.91These demographic changes are regionally concentrated, with some areas seeing particularly major changes. Today, 50% of central Bradford’s population was born outside of the UK. Between 2001 and 2021 Dagenham’s white British population fell 51%.92

Another extreme example of how rapidly immigration has changed UK communities is offered by the town of Boston in Lincolnshire.93 Following the expansion of the EU in 2004, Boston received a large number of immigrants from Eastern Europe and by 2011, 13% of the town’s population was born in the EU. In 2016, Bostonians were the most likely in Britain to vote to leave the EU, with 75% of the population voting in favour of Brexit.94

The absence of a coherent integration strategy has made these changes more difficult, with little in the way of a coordinated national policy to support the smooth assimilation of people who are newly arrived, or to actively develop community cohesion.

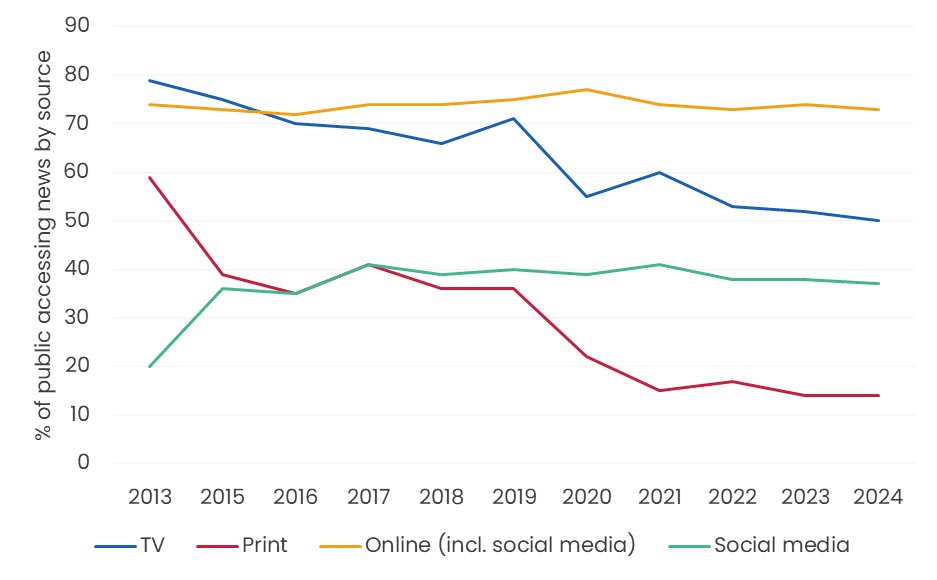

In the twentieth century, a relatively small number of news sources, from broadcasters to newspapers, were consumed by the majority of the public. But these traditional news outlets now compete with algorithm-driven social media platforms.

Figure 16: News is increasingly consumed online as more traditional means of consumption have declined.

Source: Reuters95

One effect of social media, and the older phenomenon of rolling news, has been to remake the relationship between politicians and the electorate. An important manifestation of this change are the extremely rapid feedback loops that now exist between politicians and the public, sometimes delivering near-instantaneous negative or positive reactions. On the one hand, these rapid feedback loops make politicians more sensitive and responsive to the public view. On the other hand, they give politicians less time to make the case for a policy change or decision to the public and may mean that a small proportion of the electorate that is both vocal and online have undue influence on a government’s policy and political decisions.

News content is also increasingly highly personalised, consumed via algorithm-curated apps like TikTok. Though it can facilitate highly targeted political messaging, this fragmentation also makes reaching a broader audience more difficult. This reduces the potential for shared national conversations or narratives, and complicates the building of national consensus on difficult questions.

Alongside these changes in the news and entertainment that people consume are concerns that everyday technologies like smartphones or social media apps are negatively impacting our mental health. This concern is particularly intense for younger people, with debate over whether or not the UK is experiencing a mental health crisis and whether or not government intervention on the matter is merited.

The British electorate is increasingly elderly: 19% of the population was aged 65 or over in 2022 and that is projected to rise to 27% by 2072.96 Older voters have become increasingly electorally powerful, because there are more of them and also because they are more likely to vote and to do so consistently.

This makes taking the decision to rebalancing our fraying social contract, some of which must include stopping or reducing wealth transfers towards older people, politically very difficult. This challenge encourages inertia among politicians and policymakers, who are wary of being punished at the ballot box for introducing reforms that reduce older people’s entitlements.

A political and policy environment which is tilting decisively in favour of older cohorts has served to lock in wealth transfers to older age groups, as over the past decade, tax and benefit changes have reduced working-age incomes even as they have bolstered those of pensioners.97 Even transfers to older groups which are becoming fiscally unsustainable are politically near-impossible to unwind with even modest attempts to rebalance spending met with fierce resistance.

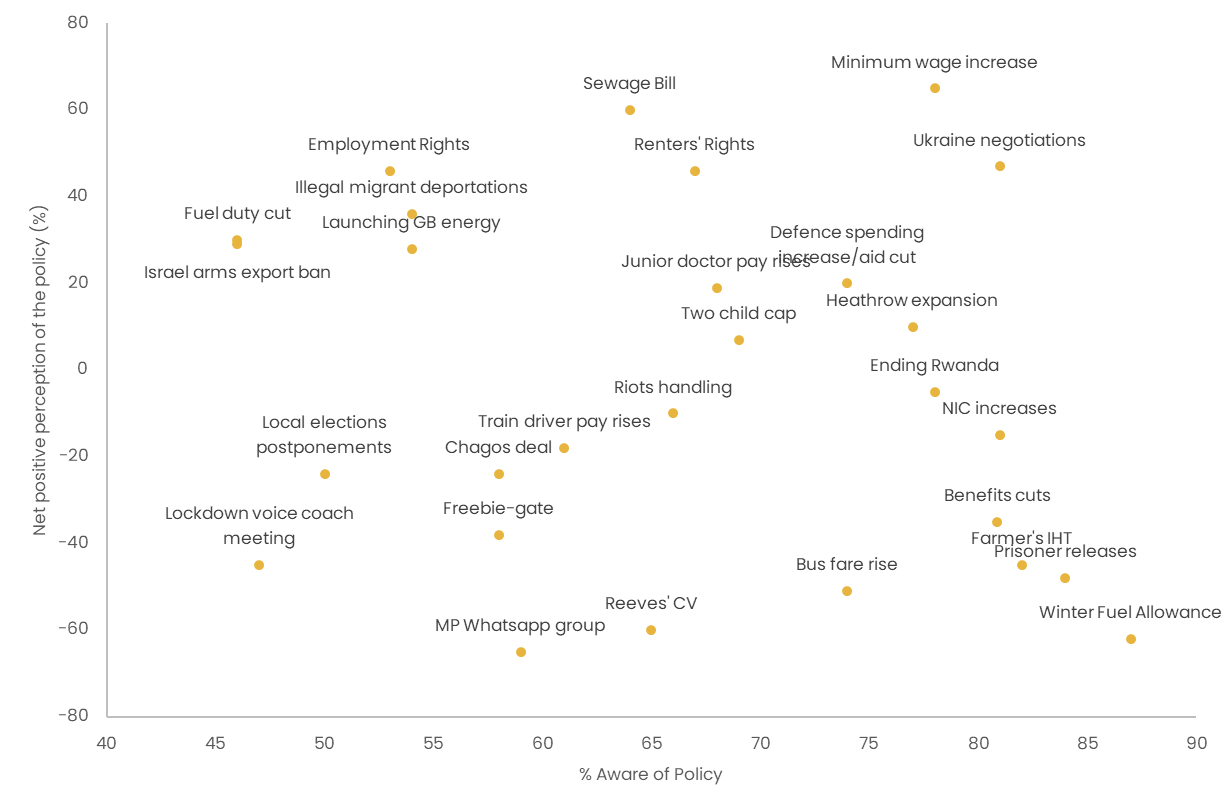

Figure 17: The Winter Fuel Payment removal has been the most contentious of any Labour policy so far.

Source: More In Common98

One of the first fiscal decisions of the 2024 Labour Government, to end Winter Fuel Payments to 10 million pensioners, was positioned by the Government as a necessary correction to spiralling costs.99 Winter Fuel Payment has been in place since 1997, brought in to address fuel poverty among older people. Today, it is younger households that see higher rates of fuel poverty.100

The decision to withdraw Winter Fuel Payment from most pensioners was immediately extremely controversial, not only because it was unexpected, but because of the Government’s rejection of a means-tested alternative, marking a significant departure from the principles of universalism that have long underpinned this welfare entitlement for older people.

Indeed the policy has faced such vehement opposition – it was identified by pollsters as the Government’s most well known and least popular policy, ahead of the early release of prisoners, cuts to welfare, and hikes in NICs – that the Government has essentially U-turned.101 Now of the 10 million pensioners due to lose the payment, 7.5 million will receive it after all.102

The Winter Fuel saga echoes the fate of the then-Prime Minister Theresa May’s ‘Dementia Tax’ in 2017. This proposal intended to reform social care funding by treating home and residential care equally, reflecting the growing property wealth of older generations by including housing assets in means-testing, while guaranteeing that no one’s assets would fall below £100,000.103

But, the policy also meant that old people receiving at-home care would have to contribute if their house was valued over £100,000, which was not previously counted in the means-test.104 This led to discontent amongst older voters and made social care reform politically toxic. The U-turn on this policy eventually came in the form of a cap on care costs, introduced in England in 2023 and set at £86,000 to limit how much people have to pay for social care over their lifetime.105

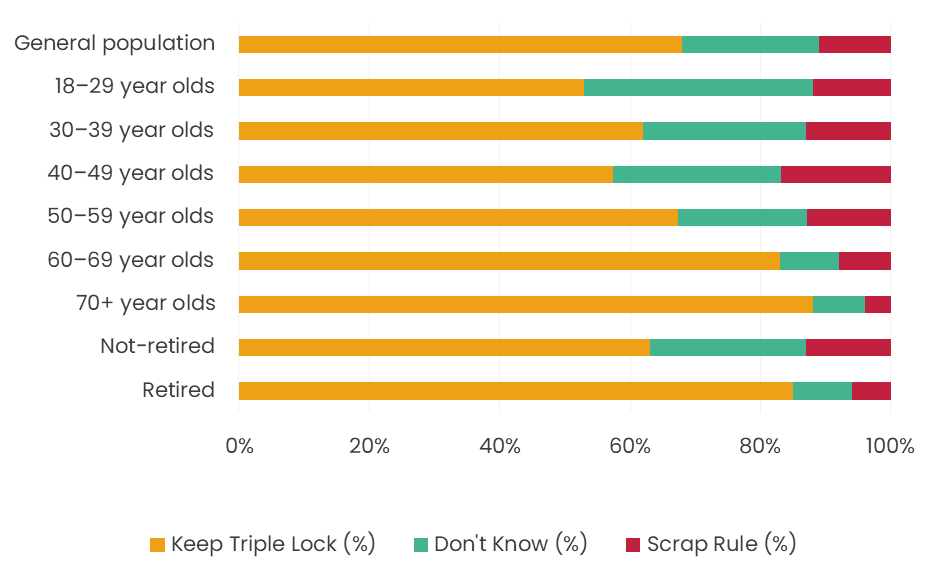

Figure 18: There is support for the triple lock across generations (as of 2021).

Source: YouGov106

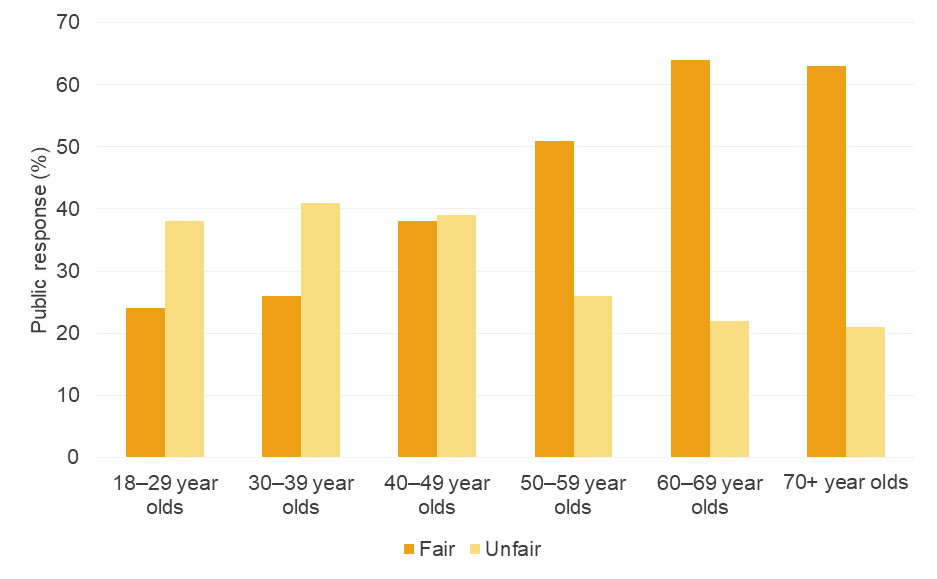

Figure 19: If average earnings are declining for workers, pension increases are perceived to be unfair by younger people, and fair by older.

Source: YouGov107

Wealth transfers from younger generations to older ones have broad, cross-generational support in principle. But economic pressures expose the dividing lines of support and fairness between working-age and older voters. 2021 YouGov polling (pre-cost-of-living crisis) showed that all generations supported the triple lock on pensions.108 But when asked if it is fair for pensions to rise when working-age incomes are falling, younger voters perceived the policy as unfair, while those over 50 viewed it as fair. Even when younger people say the triple lock is unfair, they still marginally support retaining it.109 But, younger generations are also less likely than older generations to say that they have an opinion on this question, reflecting in part the lack of political incentive to correct these fairness imbalances.110

Successive governments have allowed this norm of continued transfers to older generations to become entrenched, even as younger people face the reality of falling real incomes and a growing share of the fiscal burden. But governments hesitate to intervene to correct this imbalance, even on the grounds of fiscal necessity, as they fear the consequences of political backlash.

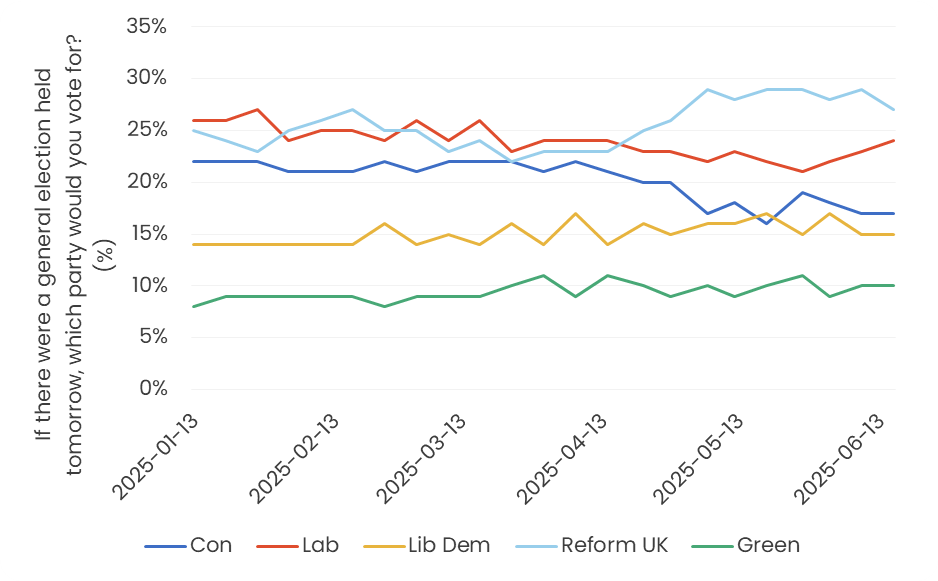

The consequences of this hesitancy is reflected in the Conservative Party’s loss of working-age voters. In 2010, the ‘crossover age’ (the age at which a voter becomes more likely to vote Conservative over Labour) was 35.111 In 2024 it was 64, an age demographic that actually fails to form a plurality in any single constituency.112 Reform UK are today polling significantly better among 18-24 year olds than the Conservative Party, particularly among young men.

Figure 20: YouGov latest polling of voting intentions, Jan 2024 to present, highlighting Conservative decline (drop to 4th) in May 2024.

Source: YouGov113

Contrary to the myth of the “grey majority,” over-65s do not form a plurality in any UK constituency, according to Onward analysis. This myth has led politicians to believe reform is electoral suicide. But constituency data shows that younger and middle-aged voters remain an important share of the electorate who may vote for change that would impact them. Electoral geography and the distribution of voters offers openings for bold, future-oriented policymaking to renew the social contract.

But the language of tradeoffs must evolve. Rather than framing change as a loss to older voters, consensus-building must stress shared gains: intergenerational investment, long-term security, and a stronger social contract. Instead of framing transfers away from pensioner benefits as an absolute loss, the state must reaffirm that it is investing in the next generation so they can better support their parents and have more children. British politics must shift from defending current distributions to building mutual, long-term security.

Rebuilding the social contract requires confronting difficult trade-offs. But these should not be framed as zero-sum losses. Policies including the expansion of homeownership and supporting family formation are not just good for the young – they underpin a more resilient state that can care for an ageing society.

The UK’s social contract is not delivering for an increasing share of citizens, as a generation of working people are being asked to pay more while receiving less. As trust in the state’s ability to deliver recedes, the state is trapped in a pincer of rising costs and shrinking revenues, particularly due to demographic pressures that successive governments have preferred to ignore rather than confront.

Renewing the social contract means having the political courage to rethink where, and in whom, the state is currently investing. It means making owning a home, starting a family, and attaining financial security again attainable for those who are working hard to contribute. It also means not branding older voters as an intransigent obstacle standing in the way of change. Instead politicians must create consensus for change by leading a national conversation about sustainability, reciprocity, and about building a system that will serve their grandchildren and great grandchildren well, while continuing to provide for older people.

No society can function if its younger people lose faith in the system. And the demographic challenges facing the UK are no passing storm. They are a permanent change in the weather and they demand a political and policy response.

Endnotes

If you value the work we do support us through a donation. Your contribution will help fund cutting edge research to make the country a better place.